(continuation. Part 2 - https://cutt.ly/j4ZOK45 )

Information failure

Information failure is a type of market failure where individuals or firms have a lack of information about economic decisions.

There are different types of information failure:

- Information asymmetries – where one party has access to information that another party doesn’t. For example, the seller of a car may know it has some problem, but the buyer may not be aware.

- Failure to disclose information. In many economic transactions, agents may not make full disclosure. For example, when applying for health insurance, you may fail to inform the insurer about genetic traits or your current ill health. When purchasing financial assets, the buyer may not be aware of the risk involved. This was an issue in the period before the credit crunch. This leads to information asymmetries

- Difficulty in estimating costs and benefits. It is often difficult to be aware of social costs of goods. Accounting costs are relatively easy to know. But, when it comes to knowing more intangible external costs, it becomes difficult to put an accurate figure.

- For example, if we take producing energy from coal powered station, the private costs to the firm can be measured in terms of labour costs, costs of coal. But, the external costs from releasing CO2 into the atmosphere are very difficult to accurately measure. It requires estimates of the monetary cost of pollution both now and in the future.

- It is also very difficult to known future costs and benefits because there are many uncertainties – e.g. what will be the real economic cost of global warming.

- Lack of education/awareness. Merit and demerit goods have degrees of information failure with consumers unaware of the true personal cost/benefit. For example, if we take tobacco, there was a time when many people were not aware of the ill-effects of tobacco on health. Recently, there has been increasing concern about the health costs of sugar consumption. Many consumers are unaware of

- the amount of sugar in processed food

- The harmful effects of sugar on health.

- Framing issues. When making decisions over whether to purchase a good, consumers will be influenced by how the good is portrayed.

- For example, a firm may advertise an orange drink has a healthy fruit drink, with added vitamin C. From the packaging a quick glance may give consumers the impression they are buying a healthy drink. But, hidden in the ingredients are very high levels of processed sugar. Drinks companies may even hide levels of sugar, by calling the sugar ‘dextrose’ or ‘glucose’. Therefore, the perception can be different to the reality.

- Moral Hazard. This occurs when individuals alter their behaviour because of certain guarantees.

- For example, an insurance firm may be willing to offer insurance against a bike being stolen. However, the firm may not realise that through offering insurance, it alters consumer behaviour and, after gaining insurance, the consumer takes less care to lock it up. Therefore, the insurance company loses out because it is more likely to pay out than previously expected.

- The government may offer a guarantee of bank deposits, but this could cause the bank to take more risks and increase likelihood government has to bail out banks.

- more on moral hazard.

- Irrelevant information / misinformation. If you are applying for a job, a firm may search on the internet and find a Facebook post from several years ago. The employer may use this and avoid giving job – even though it is no longer relevant to who you are now. Alternatively, there may be false information/slander circulated which is hard to deny.

- Information bias. The government has set up regulators to deal with natural monopolies, e.g. gas and electricity. The regulator aims to set fair prices for industry and consumers. However, if they rely on information from the firm, they may become sympathetic to the firm and allow price rises. This is known as regulatory capture – where regulators act in a favourable way to the firm they are regulating.

Possible information failures in daily life

- Are we aware of the full benefit of studying and passing exams for lifetime income and opportunities?

- Are we aware of the health costs of a full fat yoghurt – with high sugar content?

- If we are employing people, how do we know how they will perform in their job?

- Confirmation bias. Do we look for information/opinions which backs up our preconceived ideas.

Asymmetric information problem

Definition of asymmetric information: This is a situation where there is imperfect knowledge. In particular, it occurs where one party has different information to another. A good example is when selling a car, the owner is likely to have full knowledge about its service history and its likelihood to break-down. The potential buyer, by contrast, will be in the dark and he may not be able to trust the car salesman.

Asymmetric information can lead to adverse selection, incomplete markets and is a type of market failure.

When looking at a car, a buyer can only see the externals and cannot know how reliable the engine is.

Examples of Asymmetric information

Asymmetric information in financial markets

Asymmetric information is a problem in financial markets such as borrowing and lending. In these markets, the borrower has much better information about his financial state than the lender. The lender has difficulty knowing whether it is likely the borrower will default. To some extent, the lender will try to overcome this by looking at past credit history and evidence of a reliable salary. However, this only gives limited information. The consequence is that lenders will charge higher rates to compensate for the risk. If there was perfect information, banks wouldn’t need to charge this risk premium.

Asymmetric information in insurance

Another example of asymmetric information is about insurance. When insuring a good, the insurer is uncertain how well the customer will look after a piece of property. For example, if a consumer was careless with locking his bike, the insurer would not want to insure it. This problem can lead to the related problem of adverse selection.

Asymmetric information in labour markets

When employing a worker, a firm doesn’t know how hard the worker will work. The employer can look at his CV and past references, but once employed he cannot guarantee the attitude of the worker.

Asymmetric information in share dealing

Managers of companies may have inside knowledge about the fortunes of the company. With this knowledge, they may know the share of the company is either over-valued or under-valued – compared to market price.

- This is why ‘insider-trading’ is illegal as managers could use their greater knowledge to make a profit out of unknowing share traders.

Asymmetric information and adverse selection

George Akerlof was awarded the Nobel Prize in economics (2001) for his 1970 paper “The Market for Lemons,” This groundbreaking work used the second-hand car market to investigate this problem of asymmetric information between buyers and sellers. Akerlof noted it could lead to adverse selection – with the price of second-hand cars being below the equilibrium because there is an incentive to sell ‘lemons’ (dud cars) and therefore people hold back the ‘peaches’ (good cars.). People hold back selling good cars because the equilibrium price is lower than real value of their good car.

Asymmetric information can also be analysed with game theory. For example, when deciding whether to cut or increase prices, firms will be uncertain about how their rivals will behave and react. They will have to make decisions while trying to second guess how other second-hand will respond.

Overcoming Asymmetric information

- Invest in the business – give signals. With second-hand car markets, if you were buying from a one-off private buyer, you would have reasons to be suspicious about the quality of the car. However, if a second-hand car dealer invests in a large property and advertising, it is a signal that the firm intends to stay in the long-term. In this case, the firm has a greater incentive to sell reliable cars and avoid costs to its reputation. This is why the price of a second-hand car from big dealers is higher than from private seller.

- Give warranties. Another way to avoid asymmetric information is for second-hand car salesmen to give warranties for the reliability of their car.

- Employ a mechanic to test car. If you are going to buy a second-hand car for £7,000, it would be worth paying £100 to a qualified mechanic to run the car through independent tests. This would give you more information. Also, the car dealer would be wary of trying to sell ‘duds’ if you were bringing a qualified mechanic to test.

- No claims bonuses. To overcome asymmetric information in insurance, insurers will give big discounts for ‘no claims bonuses’ this is the best way of gaining better information about ‘careful’ and ‘unlucky’ consumers.

The end of asymmetric information?

Some economists argue that the internet has helped to reduce the incidence of asymmetric information. For example, when guests go to visit hotels and restaurants – they can look at online reviews to have a better idea of what to expect. Selling second-hand goods through market places like Ebay relies on sellers building up good reviews. Therefore, there is an incentive to only sell goods which are correctly marketed.

Principal-Agent Problem

The principal-agent problem is a situation where an agent is expected to act in the best interest of a principal. But, the agent has different incentives to the principal, leading to a conflict of interests.

A principal delegates an action to another individual (agent), but there are two issues. Firstly, the principal does not have full information about how the agent will behave. Secondly, the interests of the principal diverge from that of the agent, meaning that the outcome is less desirable than the principal expects.

Shareholder and manager

For example, a shareholder (principal) wants to maximise profits for his firm. He hires a manager (agent) to run the business. However, due to agency costs, the shareholder cannot fully know how hard the agent is working and to what extent the manager is fulfilling the contract. Also, in this situation, the manager does not share the same interest in maximising profits as the owner.

Market failure

The principal-agent problem can lead to market failure because the agent pursues his own self-interest rather than that of the principal and the business may be run in an inefficient way. In extreme cases, the mutually beneficial action may not happen because the principal lacks information.

The Principal-agent problem can also cause adverse selection – poor choices based on asymmetric information. This is where the agent has private information before a contract is written. For example, a lazy worker gets a job because the employer doesn’t know he is lazy.

Requirements of principal-agent problem

- Multiple actors who have a different set of objectives (e.g. shareholders vs workers.

- Asymmetric information (the agent having more information than principle.) The shareholder can see some stats like profit, but only the manager knows exactly how hard he worked or didn’t.

Examples of Principal-Agent Problem

Shareholders and managers of a company. Shareholders will wish to maximise a firm’s profits to increase their dividends. However, the manager and workers, who are responsible for day to day running of the firm, may fail to pursue profit maximisation. Instead, they concentrate on enjoying work and getting on with workers.

Landlord and tenant. The landlord owns house and rents out to tenants. He asks tenants to take care of the property and minimise electricity bills. But, tenants may open windows rather than turn down the heating.

Sub-contracting your essay. Suppose a lazy student paid a random stranger on the internet to write a dissertation. Apart from being cheating which could lead the student to be expelled, it is also an example of a principal-agent problem. The lazy student pays $500 for the essay, but the person writing the essay in anonymity has not the same motivation and may not care about the quality. They will gain $500 whatever happens to the grade.

Principal-Agent Problem and Moral Hazard

The principal-agent problem can also lead to an individual taking an excessive risk because the ultimate cost is borne by someone else. This is an example of moral hazard.

For example, an investment banker may gain a bonus for making high profits. This encourages the banker to take risky investments. If he fails and loses $700m, the losses are absorbed by the bank (or taxpayer) – not by the individual banker. This has led to major banking collapses, such as rogue trader Nick Leeson and Barings Bank (1995).

Costs of Principal-Agent Problem

Agency costs. Due to information asymmetries, principals may be unaware of how much a contract has been fulfilled. Principals may be reluctant to enter into a contract at all for the fear that they will not know what is going on. For example, a landlord may be reluctant to lend if he fears that a tenant may mistreat his property and be unable to know how it is cared for. If a mutually beneficial transaction doesn’t occur at all, this would be a significant welfare loss.

“We define an agency relationship as a contract under which one or more persons (the principal(s)) engage another person (the agent) to perform some service on their behalf which involves delegating some decision making authority to the agent. If both parties to the relationship are utility maximisers, there is good reason to believe that the agent will not always act in the best interests of the principal.”

Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure Jensen and Meckling (1976)

Inefficiency. Principal-agent problem enables agents to produce sub-optimal work. For example, managers may be profit-satisfiers – leading to higher costs and less profit.

Cost of monitoring/incentives. To try and overcome the principal-agent problem, the principal will have to spend money on monitoring and providing incentives for workers.

“However, it is generally impossible for the principal or the agent at zero cost to ensure that the agent will make optimal decisions from the principal’s viewpoint.”

Jensen and Meckling (1976)

Overcoming Performance Related Pay

Tipping. Waiters who rely on tips for pay will have their interests more aligned with owners (principals). This can be an effective way to remove the principle-agent problem. However, due to social conventions, it is difficult to move away from tipping in all but the limited industries of restaurants and cafes

Performance Related Pay. A simple solution to give agents an incentive to work hard. However, it depends on how Performance Related Pay is implemented. Without sufficient flexibility, it can create tension in the workplace and reduce co-operation. Also, some jobs are suitable for objective evaluation, e.g. fruit pickers have an easily quantifiable output. But, other jobs, such as teaching and managers require more subjective evaluation.

Different workplace environment. Workers are motivated by a variety of factors other than pay. Some of the main motivations are not pay, but pride in work and a sense of achievement. A management structure which encourages independence and workers taking responsibility for work can be more effective than crude pay bonuses.

Moral Hazard

Moral Hazard is the concept that individuals have incentives to alter their behaviour when their risk or bad-decision making is borne by others.

Examples of moral hazard include:

- Comprehensive insurance policies decrease the incentive to take care of your possessions

- Governments promising to bail out loss-making banks can encourage banks to take greater risks.

Conditions necessary for moral hazard

- There is information asymmetry. Where one party holds more information than another. For example, a firm selling sub-prime loans may know that the people taking out the loan are liable to default. But, the bank purchasing the mortgage bundle has less information and assumes that the mortgage will be good.

- A contract affects the behaviour of two different agents. In some cases, two parties face different incentives. If you are insured, then you may have less incentive to take care against risks. For example, if a country knows it will receive a bailout from the IMF, then it may feel less incentive to reduce debt. Moral hazard is particularly a problem in the insurance market because when insured, people may be more liable to lose things.

Definition of Moral Hazard

“any situation in which one person makes the decision about how much risk to take, while someone else bears the cost if things go badly.” [1]

– Paul Krugman

In the great depression of the 1930s, many American banks went bankrupt. This had a devastating impact on the economy, leading to decline in money supply, fall in output and rise in unemployment. Since this financial crisis, there has been an implicit understanding the government should bail out banks and prevent them going bankrupt.

However, this implicit guarantee to bailout banks means that banks have a greater incentive to take risks.

If risks lead to higher profit – they benefit

If risks fail and lead to bankruptcy – the banks will benefit from a government bailout.

A simplistic model of the dangers of moral hazard.

The financial crisis of 2008/09 led to many banks/large financial institutions to run short of liquidity. In the UK and US, governments intervened offering large-scale bailouts.

The problem with bailing out banks is that it creates another precedent for the future. It may encourage banks to take risks in the future.

- However, despite this problem of moral hazard, the economic costs of allowing banks to fail would be even greater.

- The solution is to try to separate banks into investment and saving branches. In other words, governments will guarantee ordinary savings, but if banks make a risky sub-prime investment, there is no need for governments to bail out this branch of bank activity.

Other examples of Moral Hazard

1. Insurance and consumer behaviour

If your bike is not insured, you will take great care to avoid it getting stolen. You will lock it carefully. However, if it becomes insured for its full value then if it gets stolen you do not really lose out. Therefore, you have less incentive to protect against theft. This becomes a situation of asymmetric information. The insurance company may assume you will look after your bike, but you may know that you won’t.

In these cases, an insurance firm faces a dilemma.

- When your bike is uninsured, it has, say, a 10% chance of getting stolen. Therefore, if the bike is worth £1,000. The cost of insurance would be based around £100.

- However, once insured, the bike may now have a 30% chance of getting stolen. Therefore, if the insurance firm charges £100 based on the 10% risk, it will lose out.

- This could lead to a missing market. The insurance firm doesn’t want to insure bicycles because people change their behaviour.

2. Moral hazard and Sub-Prime Mortgages

In the case of the sub-prime mortgage market 2000-2007; lenders faced a situation of moral hazard. They were able to sell on mortgage bundles to other financial institutions. Because there was strong demand from other people, and because other banks were taking on all the risk, the mortgage companies had less incentive to check the mortgages could be repaid. Therefore, there was a big growth in sub-prime mortgage lending with inadequate checks made.

3. Fiscal and Monetary Union

It is argued that membership of the Euro can cause a type of moral hazard. A country in the Euro may assume that if it gets into difficulties, other countries will bail it out. Therefore, they may allow their debt to grow. For example, when Greece joined the Euro, it benefited from low-interest rates because it was in the Euro. This encouraged them to keep increasing public sector debt – until markets realised too late that they actually had high, unsustainable debts.

4. Management

If managers or civil servants have a guaranteed job for life, this may alter their work incentives. If they are protected from making bad decisions, they have a greater willingness to make self-serving decisions or help out friends. This is more of a problem if it is difficult to evaluate who is accountable for the decision. It is related to the principle-agent problem and can lead to outcomes such as profit satisficing.

5. Health insurance

J. Arrow (1963) in “Uncertainty and the Welfare Economics of Medical Care,” argued that medical insurance companies may be reluctant to offer full insurance because doctors have an incentive to over-prescribe treatment – even if risky and not certain to work. Doctors will take on risky treatment because the cost is borne by others (the insurance companies)

6. Moral Hazard from IMF intervention.

Free market economists have argued that IMF intervention for countries experiencing crisis, encourages risky behaviour by countries. (Criticisms of IMF)

Overcoming Moral Hazard

1. Build in incentives. To avoid moral hazard in insurance, the insurance firm will design a contract to give you an incentive to make you insure your bike. This is why they will not insure for the full amount. Usually you have to pay the first £50 of an insurance claim. Insurance firms also make the process of getting money difficult. This means that you become more reluctant to make claims and so will try to avoid having your bike stolen in the first place.

2. Penalise bad behaviour. The government could bail out banks, but penalise those responsible for making the reckless decisions. In the case of Greece, bailout funds are being given very reluctantly and with conditions to reform and pursue austerity.

3. Split up banks so they are not too big to fail. The problem occurs when banks with consumer savings also take on risky investments. It is the risky investments which need a bailout.

4. Performance related pay. To avoid moral hazard in the labour market, there can be some form of performance evaluation and no guarantee of a job for life.

Readers Question on Moral Hazard – can it be when information is complete when information is asymmetric when information is biased against the consumer or is it when information is exaggerated?

Two parties may have good information, but the presence of a contract changes peoples behaviour, e.g. in the case of insurance. In that sense, the information isn’t really complete because the insurer isn’t aware the contract will change peoples behaviour. Exaggerated or asymmetric information can all lead to moral hazard.

It is worth being aware of adverse selection. Adverse selection occurs when there may be a bad choice of products due to asymmetric information.

Macroeconomic Instability

Readers Question: my question is whether economic instability means high and fluctuated inflation, employment and unsustainable growth or has other definition?

Economic instability can take various forms. In recent years, we have witnessed a few examples of this. The main types of instability are:

- Inflation – The cost-push inflation of the 1970s. In extreme cases, hyperinflation, e.g. Zimbabwe 2008

- Credit crunch – When the financial sector becomes short of liquidity causing a fall in bank lending, e.g. 2008/09

- Asset bubbles/bust – When asset prices rise rapidly due to irrational exuberance – but then fall.

- Economic growth/recession

- Balance of payments crisis – Countries reliant on a commodity like oil, can be adversely affected by fall in price – leading to capital outflows, e.g. Venezuela, Russia (2016)

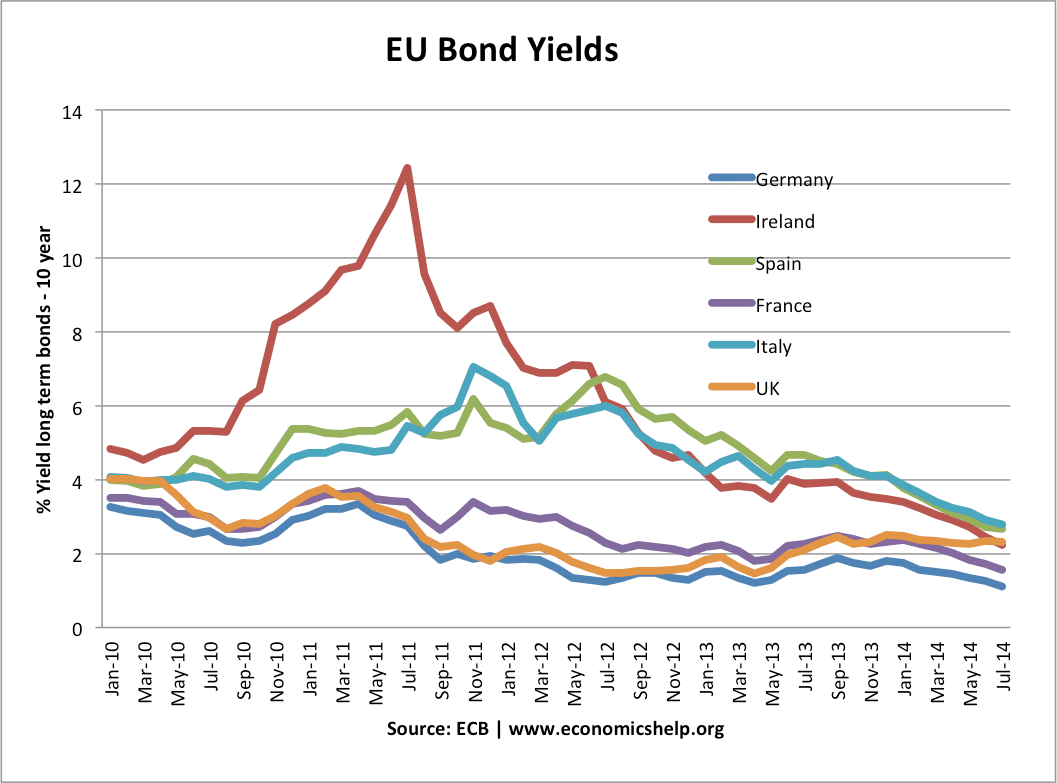

- Bond crisis – Eurozone crisis of 2012 saw a rapid rise in bond yields due to high debt and a shortage of liquidity.

More detail on Types of Economic Instability

Inflation

In the 1970s, the UK (along with other Western Economies saw inflation above 20%). This was due to higher oil prices, rising wages and inflation expectations. The high inflation created uncertainty because

When prices are rising rapidly, firms and consumers become uncertain about future costs, prices and profitability – this uncertainty tends to reduce their willingness to invest. When inflation is very high and when inflation is above interest rates, the real value of money can decline quickly causing savings to fall in value. In the 1970s, many investors who bought government bonds saw the real value of their savings decline.

Further reading – costs of inflation

Hyperinflation

In extreme cases, inflation can get out of hand and make ordinary economic transactions difficult. For example, in Zimbabwe, the government responded to a declining economy by printing money, but this caused money to rapidly lose its value.

When money loses value, economies can become very unstable as consumers have to resort to a barter economy. For example, the hyperinflation of Zimbabwe created great economic misery and a collapse in living standards. At its peak, Zimbabwe had a daily inflation rate of 98% – making ordinary transactions difficult as people lost confidence in money.

Further reading – hyperinflation

Asset Bubbles

In the early 2000s, there was a global boom in housing. Countries like US, Spain and Ireland saw rising house prices – which encouraged a boom in building. However, the asset bubble proved unsustainable and when the market turned, house prices fell. A volatile housing market affects the reset of the economy. Rising asset prices (especially housing) encourage spending as people remortgage their house. But, a fall in house prices causes this wealth effect to evaporate and people become cautious over spending. The fall in house prices in US and Europe was a significant factor behind the recession of 2009.

Bond crisis

In 2011 and 2012, the Eurozone saw a shortage of liquidity in the bond market. This caused bond yields to rise as markets were less willing to buy government bonds. This led to pressure for fiscal austerity – which in turn led to lower economic growth.

Economic growth/recession

Volatile rates of economic growth have important implications on economic stability. In a recession, with falling output, there is a rise in unemployment, poverty, fall in confidence and a rise in government borrowing. Recessions can cause firms to go out of business so they become more risk averse about investing.

Central banks endeavour to keep economic growth stable and avoid ‘boom and bust‘ cycles – where growth is rapid causing inflation, but followed by an economic downturn.

Balance of payments crisis

A balance of payments crisis occurs when a country struggles to meet foreign repayments. For example, if export revenues fall (due to falling in oil prices), there will be a rapid deterioration the current account balance of payments. This will cause a depreciation in the exchange rate. If the depreciation is rapid, it can cause individuals to try and put their money in foreign currency to protect its value. This leads to capital flight and can put further pressure on the currency. As the currency devalues, it causes inflation and increases the cost of foreign debt repayments.

The South East Asian crisis of 1997 occurred when foreign investors lost confidence in these emerging economies and sought to withdraw funds. It led to rapid depreciation and further falls in confidence.

Further reading – Asian financial crisis of 1997

Other types of economic instability

Confidence. Economic instability is linked to confidence. When the economy shows signs of instability, consumers and firms become risk-averse. Typically, when people worry about the future, they save a higher % of their income. This higher saving rate can cause a larger fall in output and more instability. It is known as the paradox of thrift.

Labour Unrest. Large-scale strikes can cause lost output and a shortage of key public services. (e.g. The Winter of discontent in the 1970s)

Banking system. When banking system ran out of credit and there was a fall in interbank lending, many realised how reliant on the banking sector the economy was.

{kind=link}

{kind=link}

{kind=link}

{kind=link}