2023 was a challenging year. Post-Covid with all its consequences: Personal issues like long-term Covid, vaccine problems, mental health, fears in uncertain times, personal economic issues, and a world in transition towards the AI era, Gen Z and Anthropocene.

Microeconomic topics on company level as the new world of work, a workforce with a request for work-life-balance and purpose, a war for talents, digitalization, implementation of AI, a clear call for sustainability and protection of our planet which includes compliance, new goals and KPIs, shortage of materials and high costs of a rising need of energy to name only a few.

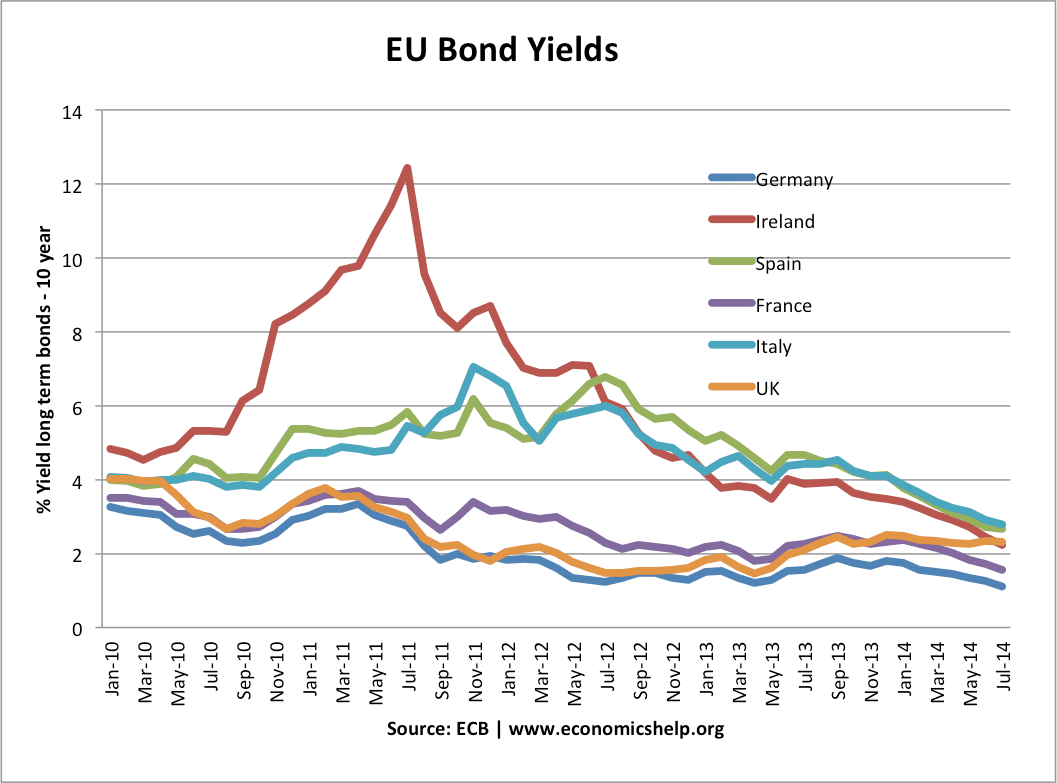

Macroeconomic and geopolitical insecurities and changes. The inflation rate will most likely fluctuate across countries and regions, depending on economic conditions, policy responses and external factors. The development of inflation will have implications for the global economy. It will affect exchange rates, interest rates, asset prices, income distribution, and the dept sustainability of many countries and regions. It will pose challenges and opportunities for both, businesses, and individuals, which will have to adapt to changing price levels. In some countries like Argentina, Turkey and Egypt inflation may reach double- and triple-digit rates.

The slowdown in China, the world´s second largest economy, trading partner of many countries, and an engine for the past four decades – based on investments, exports, and debt - will have an impact. China faces an aging population, high unemployment among younger workers, declining productivity as well as environmental challenges and a real estate crisis.

The world´s largest economy, USA is better off with a slowing inflation and a historically strong labour market. Business leaders are optimistic, whereas consumers, the general public remain rather pessimistic.

Politically, in 2024 democracy could be challenged by elections, economic uncertainties, and populist movements. In Germany, the right-wing party AfD gained about 10% voters in 2021. In the 2023 ´Länder elections` it reached up to 27,5%.

We live in a politically, economically, ecologically, and technically challenging situation. We need to be aware of these changing times, get information from different, objective sources, think critically about the options new technologies provide for the future, determine what we want for the planet and ourselves, human beings, considering that other continents may have different necessities.

We need to set norms and values, remain the protagonists of humankind: "High tech with high touch" is not only a slogan at Morgan Philips.

Given these facts and developments, what is important in leadership, what does it mean to be a good leader?

- A good leader in times of change, uncertainty and crisis needs to have a clear view of what is happening on the political, economic, and societal level. He needs to be a careful analyst, get information and be able to see the larger picture, the context, and correlations.

- He needs to be and display resilience, reflect, keep a clear vision and steady hand amidst uncertainty. This is what will be transmitted to employees and stakeholders. Positivity while being vigil and analytic.

- A leader needs to be agile and adapt to new situations and challenges. If the situation requires change, he will embrace and implement it.

- A successful leader has the capacity to inspire and motivate others even though the situation may be difficult.

- He is proactive in solving problems and making tough decisions.

- His communication is transparent and empathetic with the team.

A successful leader prioritizes the well-being of the group. He has a strong emotional intelligence. He focusses on long-term goals while navigating short-term crises, being aware that sometimes there may be a conflict of interest in respect to these goals.

The company culture is aligned to his culture and vice versa.

How can a leader address personal challenges of employees?

It is important to see, acknowledge and take care of personal issues of employees or stakeholders. Observing during lunch time. To immerse oneself once in a while, going to lunch together, being part of the group. It may be helpful to address somebody directly, showing that you care. If it overwhelms in a particular moment and you are elsewhere with your thoughts don´t ask as the intended effect may become the opposite. Rhetorical questions in a sensitive moment can worsen a situation unless they are asked on purpose to motivate a process of becoming aware. Being authentic. In some cases, you may help by sharing a personal experience or by considering options the company may offer like a healthcare plan or pension advice, counselling, or other support services. Always consider the context of the employee. Is it GenX, Y or Z? What is the cultural background, what is the family situation, and which formal education does he or she have? All these factors influence. One does not fit all, humans are individuals. Respecting this a leader will be able not only to manage diversity and help to resolve conflict situations by inspiring but get the constructive and positive aspects out of diversity. A good leader should train his managers to recognize signs of personal distress in team members and respond appropriately, including directing them to available support resources. Creating a supportive culture is crucial for a productive and efficient staff. Open and correct communication is key.

How does a leader address microeconomic topics?

Microeconomic challenges refer to issues that affect individual businesses, households, or markets, focusing on the behaviours and decisions of specific economic units. Consumer behaviour, production costs and dynamics, market structures, pricing strategies, resource allocation, government intervention, income distribution and technical changes are all factors of microeconomy: Cost increase as for labour and material, happening now due to war for talents and geopolitical conflicts that affect availability of materials and supply chains. Competition is another influencing aspect. To compensate and keep or gain back market share the leader needs to enhance innovation, reduce prices, or improve quality. As consumer demand fluctuations occur, a leader has to observe consumer behaviour, understand it, and adapt a priori to keep sales and revenue at a growing level. The challenge of regulations and compliance has gained importance with the call for sustainability, ESG and new regulations in the Life Science sector and as for digitalization.

A successful leader considers and coordinates all factors.

How to embrace the challenge of macroeconomic insecurities?

Macroeconomic aspects influence countries, businesses, and individuals, all interconnected. Inflation is a macroeconomic insecurity and beyond the influence of a single company leader. It does have an impact on the company as prices of products and services may have to be adapted. This is an entrepreneurial decision based on a market analysis. Strategic planning and financial management, price strategy adjustments, risk management. Flexibility and adaptability are required in this. Employees who are consumers on the other hand have to be supported by possible salary adjustments or additional benefits to maintain a certain purchasing power. Operational excellence plays a major role and has to be reviewed, think about supply chains.

Interest rate fluctuations may influence investment decisions of a company. A successful leader will balance an investment decision with the risk of changing interest rates. Political instability and global economic shocks like pandemics, wars or international trade disputes can cause sudden and severe impacts. A leader needs detailed, transparent and objective information – not obvious anymore -, the knowledge and experience to understand the impact and how to guide the company through these challenges. He needs to have the according education and skills.

Further macroeconomic challenges are exchange rate volatility that may impact international trade, foreign investments, and the cost of imported goods. Public dept may lead to concerns about a country´s fiscal health and its ability to meet future obligations, a psychological element. Rapid technological advancements can disrupt industries. All factors may have an enormous impact on the company, its business, and relations. They need to be seen, better foreseen, addressed and resolved by the leadership of a company.

A leader must integrate personal, microeconomic, and macroeconomic considerations when guiding a company through both challenges and opportunities for growth. Balancing these aspects requires a comprehensive approach in:

- Strategic Planning

- Effective Communication

- Adaptability

- Employee Engagement

- Risk Management

In recent years and 2024, leadership approaches are increasingly influenced by global events, technological advancements, and evolving workforce expectations. Some key aspects have become particularly relevant:

Digital fluency, adaptability and agility, emotional intelligence, inclusivity and diversity, sustainability and social responsibility, continuous learning and development, resilience and mental health, cross-cultural competency, and transparent and authentic communication.

A complex world in transition demands leaders who ask questions and analyse, who have vision and values beyond KPIs and GPD, who think critically, are humble enough to ask questions and guide successfully through challenges with knowledge, experience, intuition, inspiration, and interest towards a different world.

A well-chosen polymath with soft skills.

This leads to "Making success stories happen".

https://bitly.ws/3i4HI

{kind=link}