The analysis of welfare economics is built around the concept of Pareto efficiency. However, this efficiency criterion does not always represent a satisfactory answer. Other times, certain optimality conditions cannot be satisfied, and therefore Pareto efficiency simply cannot be reached. In order to solve this problem, and to find a new way to establish which allocation is best, economists have been since searching for new criteria to make a more informed decision.

In this Learning Path we’ll learn about some of these criteria, in order to understand them and being able to use them. In this LP we’ll learn about:

Pareto efficiency, the cornerstone of welfare economics.

Compensation criteria

Definition: what they are and how to use them. More precisely, we’ll talk about:

Kaldor’s criterion, Hicks’ criterion, Scitovsky’s criterion, Little’s criterion, and Samuelson’s criterion.

Theory of the…

Second best, a theory by economists Kelvin Lancaster and Richard Lipsey.

Pareto efficiency

Summary

The analysis of welfare economics is built around the concept of Pareto efficiency. However, this efficiency criterion does not always represent a satisfactory answer. In order to solve this problem, and to find a new way to establish which allocation is best, economists have been since searching for new criteria to make a more informed decision. In this Learning Path we learn about some of these criteria.his efficiency criterion was developed by Vilfredo Pareto in his book “Manual of Political Economy”, 1906. An allocation of goods is Pareto optimal when there is no possibility of redistribution in a way where at least one individual would be better off while no other individual ends up worse off.

A definition can also be made in two steps:

-a change from situation A to B is a Pareto improvement if at least one individual is better off without making other individuals worse off;

-B is Pareto optimal if there is no possible Pareto improvement.

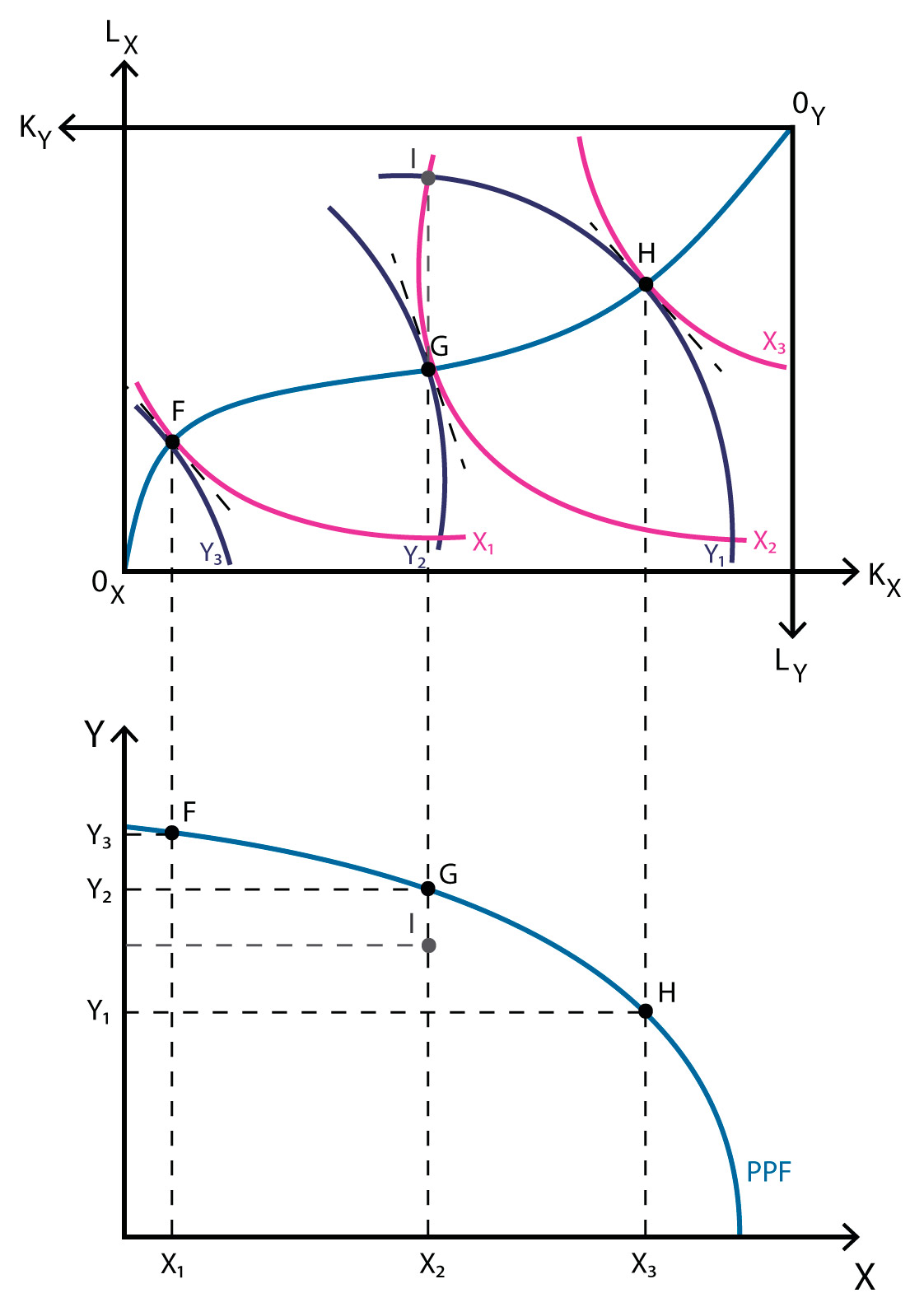

This can be easily understood using an Edgeworth box. Starting from point C, two Pareto improvements can be made:

-from C to D: individual 1 would increase its utility, since a further indifference curve would be reached, while individual 2 will remain with the same utility;

-from C to E: individual 2 would maintain its utility while individual 2 increases theirs.

Once we are at point either D or E, no further Pareto improvements can be made. Therefore, D and E are Pareto optimal.

Following the same steps for every indifference curve, we can say that every point in which indifference curves from different individuals are tangent is Pareto optimal. The curve that links these infinite Pareto optima is called the contract curve.

Video – Edgeworth box:

Pareto efficiency is great, no doubt about it, but sometimes it is impossible to reach. That’s why we need other compensation criteria. Next, we’ll see a definition of compensation criteria: what they are, how they work, and what to expect of them.

Compensation criteria

In welfare economics, compensation criteria or the compensation principle is known as a rule of decision for selecting between two alternative states. Two states will be compared; if one state provides an improvement for one part but causes deterioration in the state of the other, it will be chosen if the winner can compensate the loser’ losses until they situation is at least as good as in the initial situation. However, this compensation may not necessarily occur.

This neo-Paretian concept was developed in order to solve the dead end in which the Pareto criterion was at the moment due to its limitations. Although, in essence, the compensation principle reduces to the Pareto criterion, it values positively a wider set that allows a positive ordering without transgressing the Pareto optimal.

To this day there has not been yet a unique and definitive compensation criterion due to its limits and some of its paradoxical implication; on the contrary, a great number of similar criterions have been formulated. From them we must highlight:

Kaldor’s criterion, Hicks’ criterion, Scitovsky’s criterion, Little’s criterion and Samuelson’s criterion.

Kaldor’s criterion

The Kaldor criterion is a compensation criterion developed by Nicholas Kaldor in his paper “Welfare Propositions of Economics and Interpersonal Comparisons of Utility”, 1939. This criterion is satisfied if state Y is preferred to state X and there is such a compensation and reassignment that Y turns to Yˈ that is at least as good as X in a Pareto sense. In the following graph we consider the utility of two individuals (A on the x-axis and B on the y-axis), which we will compare using the utility possibility frontier of two different moments.

When moving from state X to Y, individual A’s utility decreases, while individual B’s increases. Individual B is willing to compensate individual A and move to Yˈ where both increase their initial utility. The opposite, moving from Y to X, can also occur if the winner, this time individual A, compensates the looser, individual B, and is willing to relocate to Xˈ.

When moving from state Y to Z, the utility of individual A decreases, while individual B’s increases. Individual B is willing to compensate individual A and go to Zˈ where both increase their initial utility. On this case the opposite, moving from Z to Y, would not be feasible.

Tibor Scitovsky pointed out some inconsistencies and the consequent limitations of this criterion which are known as the Scitovsky paradox. This paradox is centred in the phenomenon that while Y can be preferred to X the opposite can also be true, as it was previously explained. This does not give a truly asymmetric result as it could just mean that going back to the initial situation is preferred. Economy would therefore oscillate between both points.

Hicks’ criterion

When moving from state X to Y, individual A’s utility decreases while it increases for individual B. Due to this, individual A should compensate individual B so the change of states does not happen, going from X to X’, which will increase B’s utility as much as going from X to Y, while the drop in A’s utility would not be as large. The same would happen if moving from Y to X. Since this ex-ante compensation is possible, neither X is preferred to Y nor Y will be preferred to X.

When moving from state Y to Z, again individual A´s utility decreases while it increases for individual B. When going from Y to Z, there is no possible compensation from individual A to individual B, since to the left of Y the utility possibility frontier is always higher. Individual A therefore can not compensate individual B, so Z is preferred to Y in Hicks’ terms. However, when comparing movement from Z to Y, the opposite logically occurs. Individual A’s utility increases while individuals B’s decreases. Individual B would compensate individual A going from Z to Z’ , and hence Y is not preferred to Z.

If we compare this with Kaldor’s criterion we see some significant changes but still both criteria fall under the Scitovsky paradox. This paradox is centred in the phenomenon that while Y can be preferred to X the opposite can also be true. This does not give a truly asymmetric result as it could just mean that going back to the initial situation is preferred. The economy would therefore oscillate between both points.

Some inconsistencies appear when using both Kaldor’s and Hicks’ criteria, known as the Scitovsky paradox. In order to solve it, we use what is known as Scitovsky’s criterion.

Scitovsky’s criterion

Kaldor’s criterion is met when going from X to Y, Y to X or Y to Z, but not when going from Z to Y. However, Hicks’ criterion is only met when going from Y to Z. Therefore, when comparing state Y to Z, winners can compensate the loss of the losers, but losers cannot compensate the other part in order to avoid the change. This is the only case in our example where the Scitovsky criterion is met, making Z preferred to Y.

Scitovsky considered the possibility of changes in Pareto terms caused by state changes. This justified the dual requirements. Analytically,

Although this criterion brings some positive contributions, there are still only minor changes that furthermore need to meet conditions. The estimation of a potential Pareto improvement is yet to be answered. Nevertheless, the Scitovsky criterion contributes to an intransitive organisation of different states

Little’s criterion

The Little criterion was developed by Ian M.D. Little in his paper “A Critique of Welfare Economics”, 1949, and it constitutes a further step for compensation principle theory. Little criticises the separation between efficiency and distribution and he demands as in Scitovsky’s criterion, for the Kaldor’s and Hicks’ criteria to hold. Furthermore, this criterion also requires that the income distribution is not worsened by the change of states.

This criterion however, brings some limitations, as a result of its implicit value judgement. The criterion will be met, if by a change of states the positively affected individual (winner) is poorer than the negatively affected individual (loser). As an example, let’s analyse the following graph, where we consider the utility of two individuals (A on the x-axis and B on the y-axis), which we will compare using the utility possibility frontier of two different moments.

Kaldor’s criterion is met when going from X to Y, Y to X or Y to Z, but not when going from Z to Y. However, Hicks’ criterion is only met when going from Y to Z. Therefore, when comparing state Y to Z, winners can compensate the loss of the losers, but losers cannot compensate the other part in order to avoid the change. This is the only case in our example where the Scitovsky criterion is met, making Z preferred to Y. However, Little’s criterion is only met if individual B is poorer than individual A.

Samuelson’s criterion

The Samuelson criterion, sometimes referred to as the Samuelson condition, was raised by the economist Paul A. Samuelson in his paper “Evaluation of Real National Income”, 1950, and belongs to the theory of welfare economics and used as a condition for the efficient provision of public goods. This critique provides a way to avoid intransitivity problems: state X will be preferred to Y if the alternative of X, X’, is preferred to the alternative of Y, Y’.

This criterion however, brings some limitations, since it is very similar to Pareto optimality. Samuelson explains that previous compensation criteria, such as Kaldor’s, Hicks’ or Little’s, hold just because they consider partial redistribution.

Now that we know everything we need about compensation criteria, let's learn about another way to avoid looking for Pareto optimality: Lancaster and Lipsey's Second Best theory.

Second best

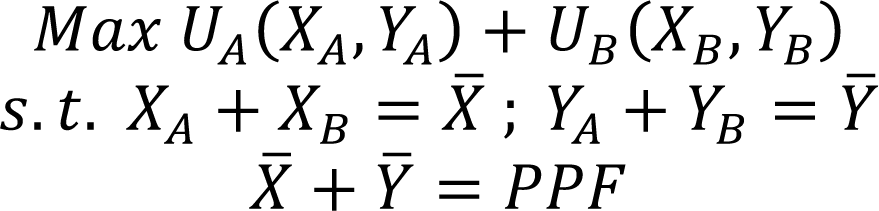

This can be easily understood using the diagram depicted in the article. We start by considering a typical optimization problem, with a given production possibility frontier (PPF) considered as a boundary condition, indifference curves (green curves, in this case representing a welfare function, ω) and the optimum where the PPF is tangent to ω (point P). Since this points lies on the transformation line and an indifference curve, it defines the production and consumption optima.

When we draw a new constraint condition (red curve), it can be easily seen that point P is no longer attainable. Q could be a second best solution, since it lies both on PPF and NewCC. However, as the authors point out, the second best point would be R, inside the transformation line. This is so because an improvement on welfare can be attained by moving to point R, since it lies on a further indifference curve (ω’’), and therefore means higher welfare.

The segment MN is technically more efficient than R, but since the points on this segment cannot be attained, R is the second best solution.

In this Learning Path we've learned about compensation criteria, used in order to avoid looking for Pareto efficiency when none can be reached. We've seen how Kaldor's and Hicks' criteria work well, except when Scitovsky's paradox appear. We've also learned about Little's and Samuelson's criteria, which keep in mind redistribution of wealth. Finally, we've seen how Lancaster and Lipsey's Second Best theory works.

https://cutt.ly/m6Tith0

{kind=link}

{kind=link}

{kind=link}

{kind=link}