Pareto efficiency

This efficiency criterion was developed by Vilfredo Pareto in his book “Manual of Political Economy”, 1906. An allocation of goods is Pareto optimal when there is no possibility of redistribution in a way where at least one individual would be better off while no other individual ends up worse off.

A definition can also be made in two steps:

-a change from situation A to B is a Pareto improvement if at least one individual is better off without making other individuals worse off;

-B is Pareto optimal if there is no possible Pareto improvement.

This can be easily understood using an Edgeworth box. Starting from point C, two Pareto improvements can be made:

-from C to D: individual 1 would increase its utility, since a further indifference curve would be reached, while individual 2 will remain with the same utility;

-from C to E: individual 2 would maintain its utility while individual 2 increases theirs.

Once we are at point either D or E, no further Pareto improvements can be made. Therefore, D and E are Pareto optimal.

Following the same steps for every indifference curve, we can say that every point in which indifference curves from different individuals are tangent is Pareto optimal. The curve that links these infinite Pareto optima is called the contract curve.

Edgeworth box

It was Vilfredo Pareto, in his book “Manual of Political Economy”, 1906, who developed Edgeworth’s ideas into a more understandable and simpler diagram, which today we call the Edgeworth box.

This diagram is widely used in welfare economics, game theory or general equilibrium theory, to name a few. It is easy to draw and can be easily explained. In the adjacent image, we can see two examples of an Edgeworth box, and how it is drawn.

The first example is mainly used for welfare economics and distribution matters. As we see, this “box” is formed using two sets of typical indifference maps, which in this case represent the indifference curves of agents A (green) and B (red), who must choose quantities of goods x and y. When the indifference map of agent B is rotated, and put on top of the map of agent A, the box is formed. When indifference curves are tangent to each other, which is the case in this example, a contract curve (blue) can be drawn using these tangency points.

Our second example is mainly used to explain Ricardian trade theory graphically. In this case, we draw the production-possibility frontier for countries 1 (green) and 2 (red). When we rotate the diagram of country 2, we end up with an Edgeworth box, which here will help understand how great the gains of international trade are and therefore helps illustrate how trade is not a sum zero game.

Video – Edgeworth box:

Production possibility frontier

The points where the isoquants of different outputs combination intersect, which are Pareto-optimal, allow us to draw the contract curve, from which the PPF can be derived. Since the technology is given, only one PPF can be derived from the contract curve (as opposed to the case of the utility possibility frontier).

Video – Production possibility frontier:

General equilibrium

A market system is in competitive equilibrium when prices are set in such a way that the market clears, or in other words, demand and supply are equalised. At this competitive equilibrium, firms’ profits will necessarily have to be zero, because otherwise there will be new firms that, attracted by the profits, would enter the market increasing supply and pushing prices down. Following the first fundamental theorem of welfare economics, this equilibrium must be Pareto efficient. Both will have a fundamental relation as a mechanism for determining optimal production, consumption and exchange.

Initial approach:

Let’s consider an economy where there are:

Two factors of production: capital (K) and labour (L).

Two goods: good X and good Y.

Two agents: A and B

The economic problem that is faced needs to find the most adequate allocation of factors of production in order to produce goods X and Y and how these goods will be distributed amongst consumers A and B. This configuration will be such that there will be no other feasible configuration that will allow an increase in any individual’s welfare without decreasing the other individual’s welfare.

In order to achieve Pareto optimality, a certain set of assumptions need to be held.

-The production function needs to be continuous, differentiable, and strictly concave. This will result in a convex set of production possibilities, also known as production possibility frontier Its shape shows an increasing opportunity cost as we need to use a higher number of resources in order to produce a larger amount of a certain good.

-Consumers’ preferences need to be monotonic, convex and continuous, showing how individuals’ welfare increases with a greater amount of goods, but with a decreasing marginal utility.

–Perfect and free availability of information.

-There has to be an absence of externalities and public goods so the utility of individuals depends directly and uniquely from their possession of goods X and Y.

Production optimisation

The optimisation problem in production relies in the maximisation of total output production taking into consideration that it is subject to a limited amount of capital and labour. Analytically,

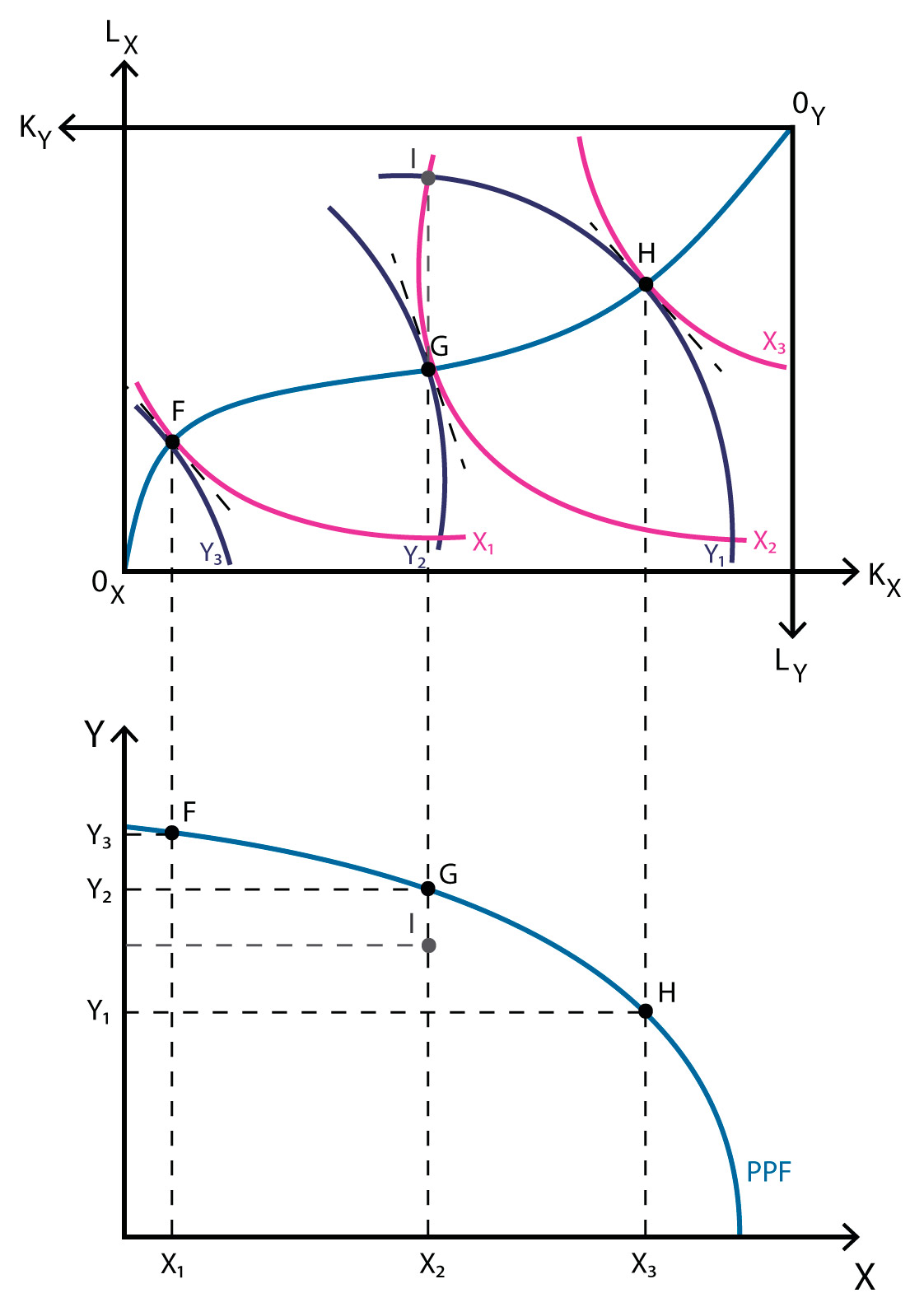

These two diagrams can be plotted together using what is known as the Edgeworth box, which makes it easier to compare quantities of capital and labour used, while also comparing quantities of goods X and Y being produced. Indeed, it’s not only easier to analyse, but also makes more sense, since the total available quantities of capital and labour are given.

{kind=link}

Graphically, if we plot all these points we construct what is known as the contract curve (blue curve in the Edgeworth box). These represent all Pareto efficient distributions, such as F, G or H. I is not Pareto efficient, since going from I to either G or H would result in an increase in the production of one of the goods without giving up the production of the other. From this curve we can derive the production possibility frontier, which shows the quantities of goods X and Y being produced, as shown in the following diagram. It must be noted that both the contract curve and its derivative, the production possibility frontier, show all the solutions that are Pareto efficient from the firm’s point of view. Only when considering input and output prices will we be able to determine a unique solution (because of the concavity of the production possibility frontier).

{kind=link}

Consumption optimisation

Bundles of goods cannot be ranked in a reliable way without knowledge of the distribution of the products, especially if a bundle has different amounts of each good. There may be some bundles that have more products of a good but less of another. The optimisation problem will be to maximise the utility of individuals A and B subject to a limited total amount of goods X and Y. Analytically,

Global optimum

Until now we have only considered different parts of the economy, and not the economy as a whole. The optimisation problem faced this time is similar to the previous one, although this time an additional restriction is added, since we are here considering both production and consumption: the production level also needs to be efficient.

{kind=link}

Competitive markets result in an equilibrium position such that it is not possible to make a change in the allocation without making someone else worse-off. In reality there are many Pareto optimums and we cannot state that one is better than the other. Even if one consumer got all of the production and the other one none, we cannot say it is an inefficient distribution if all resources are being used efficiently. This is the reason why some economists believe it is an incomplete criterion. However, there are others, such as Milton Friedman and the advocates of the Chicago School, for whom this proves that the economy will act efficiently without the need of government intervention.

Fundamental theorems

There are two fundamental theorems of welfare economics.

-First fundamental theorem of welfare economics (also known as the “Invisible Hand Theorem”):

any competitive equilibrium leads to a Pareto efficient allocation of resources.

The main idea here is that markets lead to social optimum. Thus, no intervention of the government is required, and it should adopt only “laissez faire” policies. However, those who support government intervention say that the assumptions needed in order for this theorem to work, are rarely seen in real life.

It must be noted that a situation where someone holds every good and the rest of the population holds none, is a Pareto efficient distribution. However, this situation can hardly be considered as perfect under any welfare definition. The second theorem allows a more reliable definition of welfare

-Second fundamental theorem of welfare economics:

any efficient allocation can be attained by a competitive equilibrium, given the market mechanisms leading to redistribution.

This theorem is important because it allows for a separation of efficiency and distribution matters. Those supporting government intervention will ask for wealth redistribution policies.

https://cutt.ly/B7XTS8D

Комментариев нет:

Отправить комментарий