Managing your own department is only part of the responsibilities in the world of management. Most companies have multiple departments to run the business. No matter what department you run, you should know how to interact and understand the functions of each department within a business organization. These next three lessons cover the fundamental basics of what is taught in an MBA course, including the parts of an organization that make up a business. If anyone of these particular departments are ones in which you currently work in, or would like to be a part of, you should find individualized training, which will go into more in depth detail regarding the subject matter. For continuity, we will use the point of view of how a “Customer Service Manager” might interact with the departments described in these next three lessons.

Managers spend time with other departments working on inter-department workflow processes, in daily or weekly management meetings, on conference calls, or meetings with the CEO. Your co-managers from different departments will be your allies and you want to keep them close. You should always have a cooperative relationship with your fellow management staff. This is why you need to understand, at least at a basic level, the functionalities of their departments. You want to be able to understand the basics of what they are talking about, especially when they are going over their performance goals. You also want to be able to understand what the CEO is talking about, much of which is usually financially based, and how you will be able to share the company’s vision with your department.

You will be in a much stronger position if you understand the dynamics of finance and overall business theory. It’s not merely for the sake of understanding another discipline, but in order to make sounder decisions likely to produce a greater return for your department. You can stand behind the logic, and not worry about the skills to challenge the assumption. By understanding the basic financial terms, economics, legal, ethics, sales figures, marketing strategies, customer service and operating functions, you will feel confident, and not blinded by science, when you are in management meetings. It will give you a chance to contribute more, and not be self-conscious about your lack of knowledge.

In this lesson we will be reviewing the different types of business along with an overview of ethics, economics, finance, accounting, budgets, and legal.

A business in its most basic form sells a product such as shoes, cars, and burgers, or delivers a service such as telephone, cable TV, and auto repair. The goal is to make a profit. Businesses use some combination of labor, equipment, and materials to produce products or services.

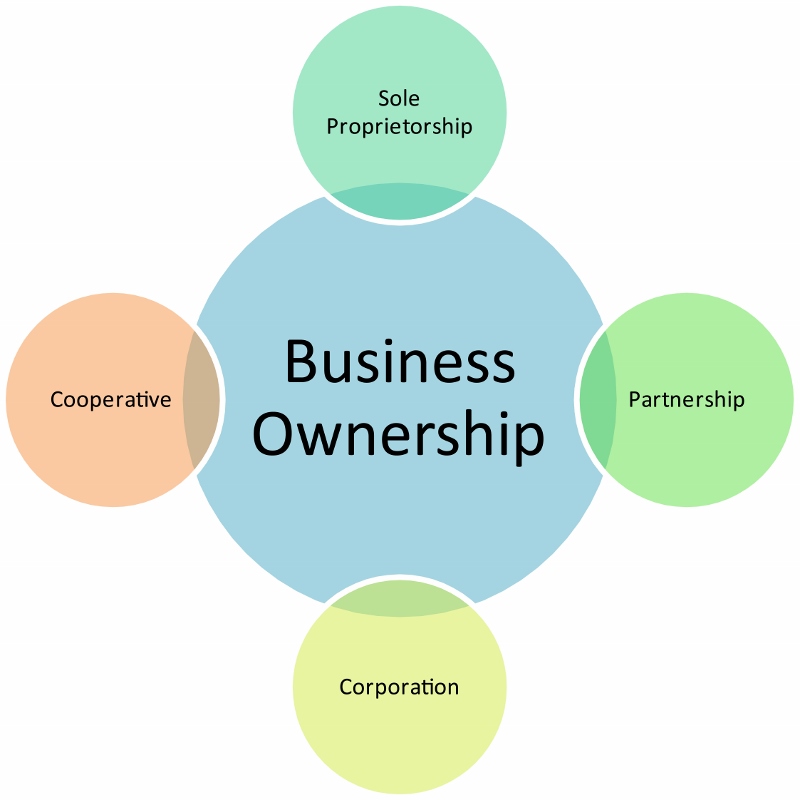

Here are the most common forms to set up a business organization, with a brief explanation of each:

Sole Proprietorship – A business owned by one person who is self-employed and has the rights to profits and is responsible for debts. The upside is full control, can sell whenever desired, and fewer regulations. The main downside is the owner is personally liable for all business debts, and it is harder to raise capital from investors. Most small businesses are organized as a sole proprietorship and will usually incorporate when the business grows in size.

Partnership – A business owned by two or more individuals who contribute funds and shares the profits and debts. Common Partnerships are accounting, law, consulting, and architectural firms.

Corporation – A business in which legally the owners are not personally liable for the financial obligations of the business. They can only lose the money they invest in the corporation. The investment is when they contribute money, or if applicable, when they buy stock in the company. A share of stock represents a share in the ownership. If the company is a publicly held corporation, the general public can also own stocks. Owners are not personally liable and a corporation is often referred to as a “legal person.” It can use the terms “Inc.” “Incorporated,” or “Company.”

Limited Liability Company (LLC) - A business authorized by state law. Although exact characteristics vary by state, the most common characteristics of the limited liability company are that it has:

1. Limited liability, that is, the owners of the company are not liable for more than the capital they have invested in the business.

2. Managed by members or managers, owners can be members or managers.

3. Limitations on the transfer of ownership.

LLC's are becoming an increasingly popular way to start a business because LLC's are generally a less complicated business structure than a corporation, and provide a significant amount of protection.

Using the same moral guidelines you already follow yourself, knowing the difference between right and wrong, also goes for business. It will tell you what is right or wrong in any business situation. Sometimes, however, what might be best for the company might seem morally wrong personally. For example, buying cheaper goods from another country will help increase the company’s profit margin, however, that country legally allows children to work for low wages. At the end of the day, businesses should be as ethically sound as they can when determining the “greater good” for all involved.

Companies that violate the more obvious ethical practices can result in huge consequences. Just look at what happened to Enron. Problems usually start off small, but build into bigger ones unless standards are truly set and followed. With the pressure to achieve the numbers, bad decisions can be made. This can be pressure on the customer service representative to wrongly fill an order, to senior management falsifying the financial health of the company.

Some business ethics, however, are much more easily recognizable as being obviously ethically wrong. To name a few:

- Money lost to Fraud

- Money lost to Embezzlement

- Accuracy of books, records, and expense reports

- Proper use of organizational assets

- Protecting proprietary information

- Discrimination

- Lying

- Over charging

- Charging for work that was not necessary

- Withholding needed information

- Abusive or intimidating behavior toward others

- Misreporting actual time or hours worked

- False insurance claims

- Kickbacks and bribery

- Proper exercise of authority

- Theft of business equipment and supplies

- Trading or accepting goods for unauthorized favors

- Moonlighting, which causes poorer work performance

- Knowingly ignoring the health and safety of employees

- Sexual harassment

- Evading someone’s privacy

Using basic common sense, if you as manager always act with integrity, you will not violate business laws or be associated with bad work ethics. This not only prevents any problems for you personally and professionally, you will also be seen and known as a solid and trustworthy leader. Make it known that everyone is expected to adhere to the highest standards of business ethics and must understand that anything less is totally unacceptable.

Standards regarding ethical behavior need to be developed, set, and communicated throughout the entire company. For more information on ethical issues, go to

www.ethics.org.

The legal department of a company takes charge of all legal matters of the company including labor laws, contracts, and legal representation. They are the team who will get involved with any legal troubles. You would have to take a course in business law to understand all of the ramifications associated with the legal department, however, we will give a brief explanation of some of the most known business laws faced by the legal department.

Basically, business law governs the rules of conduct of people and organizations in business, and is meant to enforce justice and obligation. The major areas of business law are:

Antitrust – which its laws ensure that competition remains fair by prohibiting companies from merging with one another, or acquiring one another, to form monopolies. A monopoly exists when there is only one supplier of some product or service, and can then charge whatever price it wants due to there is no longer any competition.

Bankruptcy – which laws let a company that is having financial problems seek protection from the demands of creditors. Chapter 11 of the bankruptcy code regulates liquidation, which means closing the company and selling its assets to creditors, and chapter 7 regulates reorganizations, which means a court supervised restructuring of a company while its creditors wait for payment.

Business organization – which are the laws that govern the formation of a business.

Consumer protection and product liability – which are regulations regarding products, services, and credit practices. Consumers should be able to assume that products will work and food is safe to eat, which is FDA regulated. Also a company cannot knowingly sell a product that it believes will be unsafe or harmful for its intended use.

Contracts – which are legally binding exchanges of promises or agreement between parties that the law will enforce.

Employment – which are laws that regulate the hours and conditions under which people work, such as child labor laws, sets minimum wage, and expands the rights of disabled people. You need to take all discriminatory laws associated with employment very seriously. The Equal Employment Opportunity Commission or the EEOC enforces these laws. The website is

www.eeoc.gov.

Intellectual property – which laws protect copyrights, trademarks, and patents.

Securities regulation – which is governed by the Securities and Exchange Commission (SEC). It polices the financial markets regarding insider trading, stock price manipulation, improper financial reporting, and improper and illegal practices at brokerage firms.

As manager, if you encounter any type of legal issue that you are not 100% aware of, or not comfortable with, be sure to ask your boss or the legal department for help. This includes the signing of any legal documentation. Always be careful on what you say and how you act. If you do get into some trouble, contact an attorney right away. However, common sense should always prevail, and you will be all right as long as you are ethically sound whenever any possible legal issues, such as discrimination or consumer protection, occur.

Although there are many interpretations, economics is basically “the study of what constitutes rational human behavior in the endeavor to fulfill needs and wants.”

In business, companies follow economic news to make decisions on what products to make or discontinue, when to hire or lay off employees, build or sell a factory, spend more or less on advertising, etc. Economics is a vastly huge subject and can go into a world of theories and complicated mathematical formulas. We will, however, cover some of the basics.

The foundation of economics is Scarcity, which refers to the tension between our limited resources and our unlimited wants and needs. Scarcity is the basic economic problem that arises because people have unlimited wants, but resources are limited. Because of scarcity, various economic decisions must be made to allocate resources efficiently. These decisions are made by giving up, or trading off, one want to satisfy another. For an individual, resources include time, money and skill. For a country, limited resources include national resources, capital, labor force, and technology. The most common phrase that you have probably heard regarding economics is, “Supply and Demand.”

Supply is the quantity of a product produced and offered for sale. The more buyers are willing to pay, the more incentive to increase the supply. On the other hand, the less that buyers are willing to pay, the more incentive to lower the price to decrease the surplus. For example, if the quantity supplied of the product is 30, and the quantity demanded for the product is 20, there would be a surplus of 10 products (30-20=10). The sellers would have to lower the price in order to sell excess supply.

Demand is based on price. The law of demand is basically; the higher the price, the lower the quantity demanded, and the lower the price, the higher the quantity demanded. As the price for a product rises, demand for that product will fall. On the other hand, if the sellers lowered the price for the product too much, demand would increase beyond what is supplied, and there would be a shortage. The optimal is to have equilibrium where the price point for the quantity supplied is in balance with the quantity demanded.

When the price is just right with no surplus and no shortage, supply and demand is known to be in Equilibrium. This means that the quantity demanded equals the quantity supplied. This is what economists use to look at regarding supply and demand for a product. A product is in equilibrium when the market price is set just right. If the market price drops, demand will exceed supply, thus prices will rise. If the market price increases, supply will exceed demand and prices will drop.

Basic Supply and Demand graph – The cross point is where supply and demand are in balance, or equilibrium, based on price and quantity:

Two branches of economics are Microeconomics and Macroeconomics. Microeconomics is the study of the decisions of individuals, households, and businesses in specific markets, whereas macroeconomics is the study of the overall functioning of an economy such as basic economic growth, unemployment, recession, depression, or inflation.

Microeconomics focuses on supply and demand and other forces that determine the price levels seen in the economy. It analyzes the market behavior of individual consumers and firms in an attempt to understand the decision-making process of firms and households. It studies the shifts in demand based on income and other consumer factors. An increase in income normally leads to an increase in the amount people are willing to pay for goods, thus are more prone to buy more luxury items. There are also competing substitute products or services, which can lower the price of the original.

Macroeconomics focuses on the national economy as a whole and provides a basic knowledge of how things work in the business world, for example, the impacts of money supply, interest rates, unemployment, and government deficits.

The way we usually measure the size of an economy is by its Gross Domestic Product or GDP. GDP is the value of all the goods and services produced within our borders in one year. People who study macroeconomics would be able to interpret GDP figures and how they relate to our national economy. Basically, GDP measures the size of the national economy by the total value of all goods and services produced within a nations border. This is a key economic indicator for economic growth rate, which measures how much bigger or smaller an economy is one period, compared with the same period a year ago. The formula used, and a brief explanations of the components measured in GDP, is:

· GDP = C + I + G + (Ex – IM). C is for Consumption (household spending), I is for Investments (business spending), G is for government (federal, state and local spending). "Ex" is for Export (goods shipped out of the country that made them) and "Im" is for Import (goods shipped into the country that outside countries made). You can see that if any component increases, the total GDP increases. If any component decreases, the total GDP decreases. There is a never-ending business cycle, which is a long-run pattern of economic growth and recession, also known as boom and bust, because of fluctuations in demand. Recovery always follows recession, and vice-versa. A business cycle is like the domino effect: During a recovery, consumers buy more (C or Consumption), which then means businesses invest more in equipment and staff (I or investments), etc. During a recovery, the business cycle is on an upswing and GDP growth continues. During a recession, the exact opposite is true. This is important to know because as manager, you do not want to get stuck with excess inventory or hire un-needed additional staff because you didn’t see the economic slowdown coming, or vice-versa because you do not have the goods to sell due to an increase in demand.

The Federal Reserve, also known as “the Fed,” controls the U.S. money supply. It is the central banking system of the United States. It replaces old currency with new currency, guarantees bank deposits, and governs the banking system. The Fed affects the economy by moving interest rates, selling and buying government securities, and talking about the economy (known as “moral suasion”). The Fed manages two kinds of economic policy:

· Fiscal policy, which is the spending and taxation to stimulate or “cool” the economy by adjusting taxes and spending. It can raise or lower spending and raise or lower taxes. Using an increase in government spending to ignite a recovery is called fiscal stimulus. If the government spends more than it collects in taxes, it is deficit spending. The government can lower taxes as well to ignite a recovery instead of increasing spending. The government can do the exact opposite if it sees inflation heading upward to cool off the economy by raising taxes or reduce spending.

· Monetary policy, which uses interest rates, purchases, and sales of government securities to heat or cool the economy. The Fed sets the rate for short-term loans that banks make to one another, called the Fed funds rate, and the rate that the Fed makes with loans to banks, called the Discount rate. These tend to drive other interest rates. If interest rates are decreased, that makes for easier credit to start spending and increase demand, which also makes it easier to repay the loan. If it starts to overheat heading towards inflation, then the opposite is true to cool down the economy. The Fed can also sell government securities, which are bonds or government debt, to cool an economy. The government has the consumers and businesses money, which means there is less in circulation, thus less spending and less economic growth, which would result in reducing inflation. If the Feds want to heat up the economy, they buy back the securities, then cash will be back in the consumer and businesses hands to spend, etc.

At the end of the day, the government wants a sound currency, low unemployment, and sustained economic growth.

Here are some more economic terms, and key economic indicators or trends, which are commonly used:

o Bubble - When the price of an asset rises far higher than can be explained by fundamentals.

o Business cycle - The business cycle has four stages including expansion, peak, recession, and recovery. Lastly, recovery is what happens after security prices fall and eventually go back up.

o Capitalism – Economic system based on private ownership, production, and distribution of goods. It is based on “Free Enterprise,” which means the government should not interfere with the economy. It’s about competition for profit.

o Consumer Confidence – A psychological view from consumers on how they feel about the economy and their prospects in the current and future economy.

o Depreciation - A fall in the value of an asset or a currency; the opposite of appreciation.

o Depression – A bad, depressingly prolonged recession in economic activity. The textbook definition of a recession is two consecutive quarters of declining output. A slump is where output falls by at least 10%; a depression is an even deeper and more prolonged slump.

o Housing Starts – The start of construction on new homes is an economic indicator. This is due to declining housing also means declining purchases that goes with a new home such as carpeting, appliances, drapes, electronic equipment, and labor such as painting and landscapers. There is a domino effect when housing sales are slow for both new homes and existing homes.

o Inflation - Rising prices, across the board. Inflation basically means your dollar does not go as far as it used to as it erodes the purchasing power of a unit of currency. It is usually expressed as an annual percentage rate of change. If prices raise gradually, consumers can adjust. However, rapid inflation can destabilize the economy. Prices and inflation are key economic indicators.

o Pareto principle (also known as the 80-20 rule) – This states that eighty percent of result is obtained due to 20 percent of actions. For example, 20% of the people own 80% of the wealth, or 20% of the sales force contributes to 80% of all revenue, etc. This rule can be used in just about any situation. For example, 80% of your better employees will only take 20% of your time to coach, thus the other 20% of your employees will take 80% of your time.

o Prime Rate – This is the rate on loans that a bank charges its most creditworthy corporate customers. This is set by several major New York banks. A sub-prime rate is for such companies or individuals that don't meet criteria of best market rates and have a history of deficient credit. Interest rates are a key economic indicator.

o Recession - A period of decline in a national economy over a period of time, usually two quarters of a financial year. Spending and demand decrease, making the economic climate more difficult.

o Securities - Financial contracts, such as:

Bonds, which is basically an IOU that states that if an investor lends money to the government or a corporation now, then they will pay your money back at a stated time in the future while making small interest payments to you along the way.

Shares, which is part ownership of a company.

Derivatives, which are financial assets that “derive” their value from other assets that grant the owner a stake in an asset. Such securities account for most of what is traded in the financial markets.

o Stock market – Basically, a high or raising stock market indicates a recovery is in progress and a failing market indicates recession. The Dow Jones Industrial Average (DJIA) is based upon 30 extremely large blue chip U.S. corporations, such as GE, Microsoft, and Coca Cola, and is used as a key economic indicator.

o Unemployment rate - The number of people of working age without a job is usually expressed as the unemployment rate, which is a percentage of the workforce. This is one of the key economic indicators. This rate generally rises and falls in step with the business cycle. The average goal is no lower than 4% and no higher than 8%. If it goes too much lower, then inflation usually occurs. If it goes too much higher, then the country could be headed towards a recession.

o Venture Capital (VC) – Private equity to help new companies grow. A valuable alternative source of finance for entrepreneurs, who might otherwise have to rely on a loan from a risk averse bank manager.

o Yield – The return on an investment expressed as a percentage of the cost of the investment.

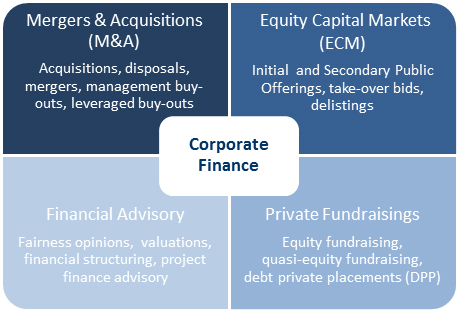

Corporate finance is the specific area of finance dealing with the financial decisions corporations make, and the tools and analysis used to make the decisions. Finance makes sure the company has the money it needs in order to operate. They are able to show external and internal parties financial data through financial statements, prepared by accountants, which are used to make decisions about the firm’s financial condition, and to advise others about possible losses and profits. Finance analyzes the health and growth of a company, manages the company’s cash, and deals with banks. Most mid to large size companies will have a CFO (Chief Financial Officer) who oversees the finance department, which normally consists of a controller, managerial accountant and/or general ledger accountant.

Finance is also involved with leasing property, equipment, purchasing raw materials, and pays employees. They provide helpful information in monitoring and evaluating management performance such as helping departments prepare their budgets and consolidate it into one company budget. They work with the Senior Management team (the CFO is part of this team) to set the company’s sales and profit goals for the year. Senior Managers use accounting information in making investment decisions, investors use accounting information to value stock, and bankers rely on accounting information in determining any potential risks to lend money.

Besides what has been previously stated, some more detailed responsibilities of corporate finance are:

- Cash flow budgeting and working capital management, which is managing the relationship between a firm's short-term assets and its short-term liabilities. The goal of working capital management is to ensure that the firm is able to continue its operations, and that it has sufficient cash flow to satisfy both maturing short-term debt and upcoming operational expenses. Working capital is: “current assets minus current liabilities.” Working capital measures how much in liquid assets a company has available to build its business.

- Comparing alternative proposals.

- Forecasting and risk analysis.

- Raise and manage its capital: Obtaining funds, debt or equity sources, long-term or short-term, and optimum capital structure.

- Allocations of funds to long-term capital investments vs. optimize short-term cash flow.

- Dividend policy.

- The risk-return framework and the identification of the asset appropriate discount rate.

- Valuation of assets. Discounting of relevant cash flows, relative valuation, and contingent claim valuation.

- The optimum allocation of funds. What to invest in? How much to invest? When to invest?

- How much money will be needed at various points in the future? How will it be funded?

- Identification of required expenditure of a public sector entity.

- Source of that entity's revenue.

We will not be able to go over each of the items just described, as you would need to take a full time financial course to fully understand it all. However, we will go over and discuss the items you might encounter whenever dealing with finance or upper management. We will present an overview of financial accounting and managerial accounting. We will discuss and have examples of two financial statements, the balance sheet and income statement. We will also discuss the cash flow statement. We’ll cover terms like Assets, Liabilities, Equity, COGS, SG&A, EBIT, EBITDA, Margins, ROI, FIFO, LIFO and Capex. And, we will demonstrate some of the most common financial analysis ratios, present a basic overview of inventory accounting, go over basic accountant responsibilities, and finally ending up with how to set up a budget.

As a manager, you should understand the basic financial statements and the associated terms in order to know how your budgets, transactions, and decisions affect the company.

Accounting provides the reliable and relevant financial information useful in making decisions. Monetary events are first identified such as the type of sales and expenses, then recorded by documenting and entering the data, and finally presented to external parties who are outside of the company, usually through financial statements, and internal parties who are the people inside the company, usually through various reports.

Financial Accounting provides information for external parties who are interested in the company’s accounting information. Examples would be reports to investors and stockholders, creditors, taxing authorities or even customers, usually through financial statements. The two most common statements are the balance sheet and income statement. This summarized data is for the entire company as a whole, and is based on a historical performance by reporting on the past. Reliability is emphasized since information is used outside the company. Financial Accounting is driven by the rules of double entry accounting in which both sides of a transaction are entered – one debit and one credit. This keeps the books in balance. For example, the purchase of new equipment will be entered as an “increase to assets,” and also entered as a “decrease to cash or increase to debt.” Since accounting information is so important on making financial decisions, rules are established to ensure that people and organizations understand how accounting information is measured. In the USA, Generally Accepted Accounting Principles (GAAP) is the common standards that indicate how to report economic events. Following standardized rules also makes sure every asset and transaction is documented, each invoice and account is paid on time, nothing is paid more than once or left unpaid, keeps all financial matters under control, and reduces the chance of embezzlement. (Note: at least two employees should be involved anytime cash is expected to change hands).

The primary purpose for the financial accounting system is to be able to develop the needed financial statements, most commonly being the balance sheet and income statement, at the end of each month, quarter or year.

Managerial Accounting provides accounting information to internal parties for profit planning and budgeting, costs of an organizations products and services, and performance reports such as budget vs. actual results. These reports are for areas or departments of the organization and not the whole company. Analyzing the data from these reports are very useful for managers who direct, plan and control its day-to-day operations, to make decisions regarding the future. Managerial Accounting focuses on the future, rather than reporting on the past. Reporting on the past is the primary role of financial accounting. Because these reports are internal, and there are no regulations, it does not follow GAAP. The institute of Managerial Accounting sponsors the CMA (Certified Managerial Accountant) and developed the standards for ethical conduct, which are competence, confidentiality, integrity and objectivity.

Costing is also a major part of managerial accounting. Knowing the cost of goods to be sold is critical before planning for the future. Using a manufacturing company as an example, the elements that go into determining manufacturing costs are:

· Direct materials or raw materials, which include any materials that become an integral part of a finished product. It is a part of COGS as a direct cost of materials needed.

· Direct Labor costs, which are costs that can be physically traced to the actual production of the product. It is a part of COGS as a direct cost making the product.

· Manufacturing overhead, which encompasses all the costs that are not designated as direct material or direct labor such as the SG&A and indirect costs like the janitor who cleans the manufacturing warehouse, etc.

Numbers are the universal language of finance and are the raw materials of a balance sheet and income statement (or P&L – Profit and Loss - statement). We will discuss all of the major financial terms and their meanings within the balance sheet and income statement in the next two sections.

The balance sheet is often described as a “Snapshot” of the current company’s financial condition on a certain date. It shows the “Assets” on the left, or top, of the balance sheet, and the “Liabilities and Owners Equity” on the right, or bottom. The Assets must balance out with the Liabilities and Owners Equity. Assets are what a company owns, such as equipment, buildings and inventory. Claims on assets include liabilities and owners' equity. Liabilities are what a company owes, such as notes payable, trade accounts payable and bonds. Owners' Equity represents the claims of owners against the business. The formula is Assets = Liabilities + Owners’ Equity.

Example – The Balance Sheet. There are explanations for each item following the Balance Sheet. Click the links on the Balance Sheet to go directly to their explanations:

| Balance Sheet - Sample Corp. Fiscal Year (FY) 2007, 2008 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 12/31/2008 | 12/31/2007 | | 12/31/2008 | 12/31/2007 | |

| ASSETS | | | LIABILITIES | and OWNERS' EQUITY | |

| Current Assets | | | Current Liabilities | | | |

| Cash | $45,000 | $40,000 | Long-Term Debt – 1 Yr. | $12,000 | $11,000 | |

| Marketable Securities | $65,000 | $60,000 | Notes Payable | $15,000 | $14,000 | |

| Accounts Receivable | $85,000 | $70,000 | Accounts Payable | $13,000 | $12,000 | |

| Notes Receivable | $45,000 | $40,000 | Taxes Payable | $11,000 | $10,000 | |

| Inventories | $85,000 | $80,000 | Accrued Expenses | $21,000 | $20,000 | |

| Total Current Assets | $325,000 | $290,000 | Other Current Liabilities | $10,000 | $9,000 | |

| | |

| Total Current Liabilities |

| $82,000 | $76,000 | |

| Land | $85,000 | $80,000 | Long-Term Liabilities | | | |

| Buildings | $100,000 | $90,000 | Notes Payable | $30,000 | $27,000 | |

| Machinery | $30,000 | $25,000 | Bonds Payable | $60,000 | $52,000 | |

| –Accumulated Depreciation | ($4,000) | ($3,500) |

| Total Long-Term Liabilities |

| $90,000 | $79,000 | |

| $211,000 | $191,500 | Other Liabilities | | | |

| Intangible Assets | | | Pension Obligations | $90,000 | $82,000 | |

| Goodwill | $15,000 | $5,000 | Deferred Taxes | $70,000 | $62,000 | |

| Patents | $20,000 | $19,000 | Minority Interest | $15,000 | $12,000 | |

| Trademarks | $15,500 | $13,400 |

| $175,000 | $156,000 | |

| Copyrights | $24,000 | $22,900 |

| $347,000 | $311,000 | |

| $74,500 | $60,300 | OWNERS' EQUITY | | | |

| Other Assets | | | Preferred Stock | $60,000 | $50,000 | |

| Investments | $25,000 | $23,000 | Common Equity | | | |

| Deferred Charges | $50,000 | $45,000 | Common Stock | $97,500 | $89,000 | |

| $75,000 | $68,000 | Capital Surplus | $111,000 | $99,000 | |

| $360,500 | $319,800 | Retained Earnings | $120,000 | $105,800 | |

| | | –Treasury Stock | ($50,000) | ($45,000) | |

| | | Total Common Equity |

| $248,800 | |

| | |

| $338,500 | $298,800 | |

| Total Assets | $685,500 | $609,800 | Total Liabilities and Owners' Equity | $685,500 | $609,800 | |

| |

| |

| |

Here is a brief explanation of the type of Assets, Liabilities, and Owners’ Equity associated with a common Balance Sheet:

| ASSETS – which is everything the company owns. They are listed in order of their liquidity, which means how easily they can be converted into cash. Current assets are first, then non-current assets, and finally all other assets. Here are the most common types of assets: | Back | |

| Cash, both in checking and savings along with petty cash. | Back | |

| Marketable Securities, which are short-term investments, like U.S. Government securities or the commercial paper of other firms. These often earn higher interest than checking or savings accounts earn. | Back | |

| Accounts Receivable, which is money owed to the company by its customers, usually within 10 to 60 days. There is usually also some bad debt, around 2%, that gets written off. For example, a customer who purchased your product but never paid. | Back | |

| Notes Receivable, which is money due from debtors. | Back | |

| Inventory, which is the goods for sale to customers, or goods in the manufacturing process. | Back | |

| · The inventory for a Manufacturer would be the raw materials to make its products, the unfinished products still being made, and the finished goods that are awaiting sale. | |

| · The inventory for a Retailer would be just the finished goods. They would not deal with the raw materials or have a unfinished product. | |

| · The inventory for a Service company would have little to no inventory on their balance sheet due to the nature of the business. | |

| Long-Term Assets or Tangibles, also known as “Fixed Assets.” The land, buildings, factories, and warehouses, including the machinery, furniture, computers, and fixtures that are owned by the company. These assets can depreciate, or lose value, on each year’s balance sheet due to age, etc. | Back | |

| · Accumulated depreciation is a way to allocate, which means assigning, the cost of a fixed asset with a life of over one year. The cost of the asset is charged against income over the life of the asset rather than all in one year. This is also known as a “contra account,” which in essence carries a minus sign. | Back | |

| Intangible Assets, which are non-physical products like patents, which are exclusive legal rights granted to an investor for a period of 17 years, trademarks, which are distinctive names or symbols granted for 28 years with option for renewal, goodwill, which is the amount of money paid for the asset above the value it was assigned by the previous owner, and copyrights, which is a form of intellectual property that gives the creator of an original work exclusive rights for a certain time period. | Back | |

| Investments, Prepayments and Deferred Charges, which is monies already spent, that will yield benefits in upcoming years like insurance coverage, rent, etc. | Back |

|

| LIABILITIES – which is everything the company owes, mostly to suppliers and creditors. Current liabilities are those payable within a year of the date of the balance sheet. Here are the most common types of liabilities: | Back | |

| Long-term debt, which is the debt due after one year of the date of the balance sheet. | Back | |

| Notes Payable, which are short-term borrowings that are payable within the year. It is a promissory note, which is basically a written promise to pay. | Back | |

| Accounts Payable, which is the amount the company owes to suppliers. | Back | |

| Federal income taxes, and when applicable city and state taxes. | Back | |

| Accrued Expenses Payable, which is all other monies, owed at the time of creating the balance sheet including employees, contractors, utilities, etc. | Back | |

| I.e. Current portion of long-term debt, which is the amount due within a year from the date of the balance sheet. This would be considered a current liability. | Back | |

| Notes Payable, which are non current (due after 12 months) borrowings. It is a promissory note, which is basically a written promise to pay. | Back | |

| Bonds payable, which is the obligation due on maturity of bonds. | Back | |

| Pension obligations, which is the liability for future pension benefits due to employees. | Back | |

| Deferred Taxes, which are the longer-term tax obligations that have been deferred to some future period. | Back | |

| Minority interest, which is the ownership of minority shareholders in the equity of consolidated subsidiaries. | Back |

| OWNERS' EQUITY (also known as Stockholders’ Equity - when applicable) – which is the amount left over for the company’s owners after the liabilities are subtracted from the assets. The formula is “Assets – Liabilities = Owners Equity.” This is also referred to as “Net Worth.” If the company is incorporated, they can issue stock. Stocks represent ownership in a corporation. A share of stock is one unit of ownership. Investors buy stock to share in the company’s profits, where as the company issues stocks to raise money from the investors. If the company is not incorporated, such as a Sole Proprietor, they will not have accounts for stock, but will invest the money back into the company through “Retained Earnings.” If this number is zero or negative, then the company is obviously in trouble and steps will need to be taken, or else there is the chance of bankruptcy. | Back | |

| Preferred Stock, which is a type of stock that pays a dividend. It is a payment from profit made to stockholders out of the company’s income at a specific rate, regardless on how the company performs. Owners of preferred stock do not have voting rights such as who should be on the Board of Directors or whether or not to sell the company. They only get dividends if the company has earnings to pay them. It is called preferred because the dividend must be paid before dividends are paid on the common stock. | Back | |

| Common Stock, which the owners have voting rights, but do not receive dividends at a fixed price. The value of the stock can rise or fall. | Back | |

| Capital Surplus, also known as “additional paid-in capital,” is the amount paid to the company in excess of the par value. When a company issues a stock, the stock has a par value, a value assigned to a share of stock by the company. This value does not determine the selling price, or market value, of the stock. The selling price that the investor pays per share is determined in the market. | Back | |

| Retained Earnings, which is money reinvested into the company and becomes part of the capital that finances the company. | Back | |

| Treasury stock, which is stock in the company that has been repurchased and not retired. | Back |

As you can see, the “Total Assets” for each year equaled the “Total Liabilities Equity.” It is called a “Balance Sheet” because it has to balance. Each dollar value was a “Snap-Shot” on the date of the financial statement. Assets are in order of their liquidity and how fast they can be converted into cash. Current assets are expected to be liquidated within one year of the date of the Balance Sheet. Liabilities and Equity are in order in which they are to be paid. Current Liabilities are payable within one year. Also, as you can see, there are two years of figures on the balance sheet for comparison and trending purposes.

Managers seeking to lead their department must learn to read between, above, and around the numbers to uncover two key indicators: proportion and direction.

Proportion: Your company’s financial reports reveal interesting and important information on the proportion of physical assets (plant and equipment) versus cash flow. This is important because the speed at which a company turns over its assets reveals how capital-intensive (requires large amounts of money) that business is. If you turn over assets quickly, you can afford low margins (profit) per sale. If you turn over assets slowly, you must earn a steep margin per sale. The key point here is if you turn over assets slowly, and earn little profit per sale, you will not be adequately profitable. It’s the proportion of cash flow versus physical assets on the balance sheet that tells you how hard you have to work those physical assets to make an adequate profit. The larger the investment in assets one has to make in a business in relation to sales, the greater the margin one needs to make on each sale.

Direction: A general sense of a company’s direction can be assessed from its financial statements. Sometimes relationships between a company’s resources and its sales growth get out of whack. If a company must invest a disproportionate amount of assets for each dollar of sales increase, then the company will be pouring extra money into its assets to such an extent that it will eventually run out of money. For example, if a company wants to grow by 20% on a sustainable basis, management must continue to add 20% to the retained earnings. This is reflected in the balance sheet in the shareholders equity. If shareholders equity grows by only 10% at a sustainable level, the company can grow by only 10% at a sustainable level. The only way to exceed 10% growth is to increase profitability or acquire additional debt (borrow more money). This is why it is so important to understand how to read the balance sheet so you can see a snapshot of the company’s direction.

Income statements show the results of a company’s operations, which are usually given quarterly or by fiscal year. It shows the sales, also known as revenue, and expenses. It also shows whether the company had a profit or loss during that period. The Income Statement is also known as the “Profit & Loss” statement or “P&L.” Simply put, the formula is: “Revenue – Expenses = Income.” The easiest and best scenario is, “The higher the sales and the lower the expenses, the greater the income.” There are all types of expenses that are generated in a company and this statement sees how the company is spending its money, and how management is most and least effective.

As previously described, the Balance Sheet shows the value in the company’s accounts at a certain period, whereas the Income Statement covers operations over an entire period.

The income statement gives you the “Net Income,” also known as “The Bottom Line,” after all costs and expenses have been subtracted from all possible income including total sales, interest earned on investments, and sale of a non-tangible item like a patent.

Example – Income Statement. There are explanations for each item following the Income Statement. Click the links on the Income Statement to go directly to their explanations:

| Income Statement | |

| Sample Corp. FY 2007, 2008 | |

| Figures USD | 2008 | 2007 | |

| |

| Sales (Revenue) | 15,500,000 | 14,625,000 | |

| Less: Cost of Goods Sold (COGS) | (9,900,000) | (10,500,000) | |

| Gross Income | 5,600,000 | 4,125,000 | |

| Less: Selling, General, Administrative Costs (SG&A) | (3,300,000) | (2,350,000) | |

| Operating Income Before Depreciation (EBITDA) | 2,300,000 | 1,775,000 | |

| Less: Depreciation, Amortization, Depletion | (11,000) | (10,000) | |

| Operating Income (EBIT) | 2,289,000 | 1,765,000 | |

| Less: Interest Expense | (93,000) | (89,000) | |

| Non-operating Income | 2,196,000 | 1,676,000 | |

| Less: Non-operating Expenses | (42,000) | (40,000) | |

| Pretax Accounting Income | 2,154,000 | 1,636,000 | |

| Less: Income Taxes | (1,350,000) | (1,240,000) | |

| Income Before Extraordinary Items | 804,000 | 396,000 | |

| Less: Preferred Stock Dividends | (87,000) | (85,000) | |

| Income Available for Common Stockholders | 717,000 | 311,000 | |

| Less: Extraordinary Items | (18,000) | (15,000) | |

| Less: Discontinued Operations | (400,000) | (100,000) | |

| Adjusted Net Income | 299,000 | 196,000 | |

| Earnings Per Share (200,000 shares of stock) | $1.50 | $0.98 |

|

| Here is a brief explanation of the type of accounts associated with a common Income Statement: | |

| Revenues – also called “Sales, “Sales Revenue,” or “Sales of Goods or Services.” It is also known as the “Top Line.” It is the amount of money the company made, before any expenses, on its operations. This, however, would not pertain to any income made from selling plant equipment or interest on marketable securities, etc. When applicable, income other than what is considered revenue is shown in “Other Income or Interest Income.” | Back |

| Cost of Goods Sold – also known as, and pronounced, “COGS” or “Cost of Sales” – These are direct costs or direct expenses because they are directly associated with making what the company sells (i.e. manufacturer), cost directly associated with the service the company supply’s (i.e. Internet Service Provider), or what a company would pay for merchandise it sells in stores (i.e. retailer). For example: | Back |

- If the company were a manufacturer, the COGS would be the cost of materials and the wages for those making the product, along with the factory operational costs associated with the product like freight and transportation, rent, power, lights, maintenance, etc.

- If the company is a service-related business, COGS represents the cost of services rendered or cost of revenues.

- If the company were a retailer then the COGS would be the price paid to the suppliers for the merchandise it sells in the stores, including the transportation costs of getting the goods into the stores.

|

|

| Gross Income – also called “Gross Profit.” It is the money the company earns on its sales before SG&A. | Back |

| Selling, General, and Administrative Expense also known as “SG&A” – It is the salary of the sales people and the commissions, sales expenses, marketing expenses, managers salaries and benefits, office expenses like the power, lights, rent, supplies, and everything else needed to run a company. This also includes the cost of the supporting departments like HR, IS, Finance, etc. Basically SG&A is all costs that are not directly producing the product, or after a retailer buys a product from a supplier, as described in COGS above. | Back |

| Operating Income Before Depreciation - This is gross income or gross profit minus SG&A. This is also the EBITDA number. For more information on EBITDA, see the related ratio explanations later in this lesson. | Back |

| Depreciation Expense – This is the amount of depreciation charged against sales during the period. This is not the same as accumulated depreciation on the balance sheet, as that is the total of all past depreciation. This depreciation expense will be on the income statement, and also added to the accumulated depreciation on the balance sheet at the beginning of the period. | Back |

Operating Income – Gross income minus SG&A gives you the operating income. This is also considered EBIT or operating profit. For more information on EBIT, see the related ratio explanations later in this lesson.

Back

Interest Expense – This item reflects the costs of a company's borrowings.

Back

Non-operating Income – An example of this would be money won from a lawsuit. Another example would be interest made on marketable securities. This is also called extraordinary or nonrecurring income.

Back

Non-operating Expenses – This could be the cost of litigation or settlements paid in lawsuits, closing down a division, etc.

Back

Pre-Tax Accounting Income – Also known as “Income Before Taxes.” This is the income before taxes.

Back

Provision for Income Taxes – Taxes that will be charged against the income in this period, even if they have not been paid in this period. This will be the income tax charged to income for the period.

Back

Income before Extraordinary Items – This is the pre-tax minus income tax.

Back

Preferred Stock Dividends - Each share of preferred stock is normally paid a guaranteed, relatively high dividend and has first dibs over common stock at the company's assets in the event of bankruptcy. In exchange for the higher income and safety, preferred shareholders miss out on large potential capital gains (or losses). Owners of preferred stock generally do not have voting privileges

Back

Net Income Available to Common Stockholders - The net income applicable to common shares figure is the bottom-line profit the company reported. To get the basic earnings-per-share [Basic EPS] figure, analysts divide the net income applicable to common by the total number of shares outstanding.

Back

Extraordinary items - Are events that occur infrequently and are unusual. They can include acts of God as long as they rarely occur in the area where the business operates.

Back

Discontinued operations - Occur when a significant segment of a business has been identified for disposal. Once so identified, any gain or loss from operations of the segment while it is being disposed of and any gain or loss on the sale of the assets of the segment, are reported separately from the remaining, continuing operations.

Back

Net Income or (Loss) – This is also known as, “The Bottom Line.” Net income is what’s left after subtracting the COGS, SG&A, and all the rest of the expenses and taxes on the income statement. Of course, if expenses exceed income, this account caption will read as a net loss. The dollar amount would be in parentheses and/or in red. For more information, see the related ratio explanations later in this lesson.

Back

*Comprehensive Income is fairly new (1998) and takes into consideration the effect of such items as foreign currency translations adjustments, minimum pension liability adjustments, and unrealized gains/losses on certain investments in debt and equity.

Earnings Per Share (EPS) - This is Net income remaining for stockholders ÷ Common shares outstanding, also considered part of the bottom line. In this example for 2008, $299,000 (Net income) ÷ 200,000 (200,000 shares of stock) = $ 1.50 per share.

Back

Income statements are like a management report card. It lets you investigate where sales are rising or falling, whether costs are rising or falling faster or slower than sales, if interests expense is rising or falling year to year, of if there were any extraordinary changes, etc. For example:

- A manager of a department who produces a product can do their part by keeping control of COGS by always being aware, and trying to reduce, the cost of materials, parts, hardware, etc.

- ·A manager of customer service would be able to reduce their part in SG&A by reducing overtime, unnecessary office space expansion, supplies, etc.

- Also, you can do a basic calculation on revenue per employee (divide the revenues by the total number of employees), and calculate the net income per employee (divide the net income by the number of employees). If you see a downward trend, then it could mean that the company is not effectively managing its employees.

|

|

|

If you're a recent graduate from any Business Management School or anywhere else in the country, our free online management training and leadership skills course will teach you management concepts, leadership styles, and the fundamentals of a mini-MBA business management certifications program.

Statements alone will let you see dollar amounts; however, you also need to analyze these statements by relating the account values to one another. Financial ratios are the most common way to do this. A ratio is a calculation of just a simple division problem that shows the relationship between two values. Financial ratios are used to show the relationship of two financial statement accounts to measure a company’s performance, and whether it is creditworthy. Here are a few of the most common ratios so you can get an idea on how it all works:

LIQUIDITY RATIOS

Liquidity ratios demonstrate a company's ability to pay its current obligations. Some of the best-known measures of a company's liquidity include:

Current ratio = Current Assets ÷ Current Liabilities: Also known as working capital ratio. It measures the ability of a company to pay its near-term obligations. The general rule of thumb is a current ratio of 2.0 or better. Using the balance sheet example shown earlier for the year 2008, the total current assets of $325,000 with $117,000 in current liabilities would have a 4.2 current ratio ($325,000 ÷ $82,000 = 4.2).

Quick ratio = Quick Assets (cash + marketable securities + receivables) ÷ Current Liabilities: Also known as an acid test. This is a stricter definition of the company's ability to make payments on current obligations. Ideally, this ratio should be 1.0 or better. Using the balance sheet example shown earlier for the year 2008, the cash plus the marketable securities plus the account receivables would equal $195,000 ($45,000 + $65,000 + 85,000) with $82,000 in current liabilities. The quick ratio is 2.4 ($195,000 ÷ $82,000 = 2.4).

Accounts Receivables Turnover = Net Sales ÷ Accounts Receivable: Also known as Sales to Receivables. It measures the annual turnover (the number of times the receivables went through a cycle of being created and collected, thus turned over, in a period) of accounts receivable. Essentially, Accounts Receivable Turnover is the average amount of time that it takes a given client or group of clients to pay outstanding invoices after they are generated and mailed to the customer. It is best to use average accounts receivable to avoid seasonality effects by adding the AR at the beginning of a period from the balance sheet to the AR at the end of a period, and divide the sum by two. A high number reflects a short lapse of time between sales and the collection of cash, while a low number means collections take longer. Using the income statement and balance sheet examples shown earlier for the year 2008, the Sales is $15,500,000 with $85,000 in accounts receivable (on the balance sheet). The Accounts Receivables Turnover = 182 times ($15,500,000 ÷ $85,000 = 182). See the Collection Period below to associate this turnover number with the average number of days it takes the company to collect its receivables.

Collection Period = 365 ÷ Accounts Receivables Turnover: This measures the average number of days the company's receivables are outstanding between the date of credit sale and collection of cash. For example, the turnover as described above is 182 times. The result would be 365 ÷ 182 = 2 average days to pay. Whether this is good or bad depends on the industry norms and credit terms established.

Annual Inventory Turnover = COGS for the Year ÷ Average Inventory Balance: This shows how efficiently the company is managing its production, warehousing, and distribution of product considering its volume of sales. Higher ratios, over six or seven times per year, are generally thought to be better, although extremely high inventory turnover may indicate a narrow selection and possibly lost sales. A low inventory turnover rate, on the other hand, means that the company is paying to keep a large inventory, and may be overstocking or carrying obsolete items. For example, the COGS from the income statement are $9,900,000 and the Average inventory balance on the balance sheet is $85,000. The Annual Inventory Turnover = 116 ($9,900,000 ÷ $85,000 = 116). See the Inventory holding period below to associate this turnover number with the average number of days that elapse between finished goods production and sale of product.

Inventory holding period = 365 ÷ Annual Inventory Turnover: Also known as Days’ Sales on Hand. This calculates the number of days, on average, that elapse between finished goods production and sale of product. For example, lets say that the turnover as described above is 116 times, then the result would be 365 ÷ 116 = 3.1 average days worth of sales in inventory. Whether this is good or bad is the comparison with the industry norms.

LEVERAGE RATIOS

Leverage Ratios are used to understand a company's ability to meet it long term financial obligations. These can also be considered as Solvency Ratios which measures the capability of a compnay to pay its bills on time.

Debt-to-Equity ratio = Total Liabilities ÷ Total Owners' Equity: This indicates what proportion of debt (trade credit, liabilities, and borrowings) and equity (shareholders purchased stock and earnings reinvested into the company rather than taken as dividends) that the company is using to finance its assets. A company is generally considered safer if it has a low debt to equity ratio. In general, debt should be 1.0 or less which means that half of the company’s total financing, or less, comes from debt. Using the example from the above balance sheet for 2008, the Debt-to-equity ratio would be 1.0 ($347,000 ÷ $338,500 = 1.0).

Debt ratio = Long Term Debt ÷ Total Assets: This compares the company’s long-term debt to the company’s total financial resources. A debt ratio greater than 1.0 means the company has negative net worth, and is technically bankrupt. Using the example from the above balance sheet for 2008, the debt ratio would be 0.13 ($90,000 ÷ $685,500 = 0.13). This tells us 13% of the company’s total financial resources are in the form of long-term debt. The lower the number the better, and if it starts to reach 50%, you want to be sure the company has a reliable earnings stream.

Earnings Before Interest and Taxes (or EBIT, pronounced e-bit) = Revenue - Operating Expenses or OPEX: This is not a ratio, however, it is important and needs to be explained before going on to other ratios (it is also a non-GAAP metric). EBIT is an indicator of a company's profitability, calculated as revenue minus expenses, excluding tax and interest. It is used quite frequently in business financial conversations with the goal to become EBIT positive. EBIT is also sometimes referred to as "operating earnings," "operating profit," and "operating income," which can be found on the income statement. Using the example income statement above for the year 2008, it would look like: $15,500,000 (Revenue) – $9,900,000 (COGS) - $3,300,000 (SG&A) - $11,000 (Depreciation) = $2,289,000

Earnings before interest, taxes, depreciation and amortization (or EBITDA pronounced E-bih-dah): The same as EBIT, however, it takes the process further by removing two non-cash items from the equation; depreciation (meaning the gradual reduction of the value of a tangible item) and amortization (meaning the gradual reduction of the value of a non-tangible item). EBITDA is used when evaluating a company's ability to earn a profit, and it is often used in stock analysis. Using the example income statement above for the year 2008, it would look like: $15,500,000 (Revenue) – $9,900,000 (COGS) - $3,300,000 (SG&A) = $2,300,000

Times Interest Earned (TIE) Ratio = Earnings Before Interest and Taxes (EBIT or Operating Income) ÷ Interest Expense: Also referred to as "interest coverage ratio" and "fixed-charged coverage." A metric used to measure the company's ability to pay the interest on long-term debt. You use EBIT because you want to measure the capability to pay the interest expense out of operating income before you deduct interest out of that income. You use income before taxes because interest is tax-deductible. In general, a higher interest coverage ratio means that the small business is able to take on additional debt. EBIT of at least three to four times interest earned is considered safe. Bankers and other creditors closely examine this ratio. Using the dollar amounts from the EBIT example above, and the interest earned from income statement for 2008, would look like: TIE = $2,289,000 ÷ $93,000 (which is 25 times).

PROFITABILITY RATIOS

Profitability Ratios are used to assess a business's ability to generate earnings as compared to its expenses and other relevant costs incurred during a specific period of time. For most of these ratios, having a higher value relative to a competitor's ratio, or the same ratio from a previous period, is indicative that the company is doing well.

Gross Margin = Gross Income ÷ Net Sales (Revenue): Also known as Gross profit. Gross margin is the gross income as a percentage of sales. This measures the margin on sales the company is achieving. It can be an indication of manufacturing efficiency or marketing effectiveness. You get the gross income by subtracting the COGS from the Sales on the income statement. Using the example income statement above for the year 2008 to get the gross margin, it would look like: $5,600,000 (gross income) ÷ $15,500,000 (revenue or sales) = 36% (which translates to 64% of its sales spent on COGS). The higher the gross margin the better. It depends on the value of the product. It could be charging more money for a high quality product while maintaining relatively steady COGS, or by offering something a customer values that can be made cheaply.

Operating Margin = Operating Income (aka EBIT) ÷ Net Sales (Revenue): Operating margin measures the operating income as a percentage of sales. If there is a good gross margin, but poor operating margin, most likely there is mismanagement that accounts for SG&A expense. Using the EBIT example and revenue from income statement above for the year 2008, to get the operating margin it would look like: $2,289,000 (EBIT or operating income) ÷ $15,500,000 (revenue or sales) = 15% operating margin. Again, the higher the profit margins the better.

Net Margin = Net Income ÷ Net Sales (Revenue): Also known as Net profitability. This measures the overall profitability of the company, or the bottom line, as a percentage of sales. A net margin range of around 5% is common, however, somewhere around 10% would be excellent. In general terms, net margin or profitability shows the effectiveness of management. Though the optimal level depends on the type of business, the ratios can be compared for firms in the same industry. The net income would be on the bottom of the income statement (this figure is the revenue minus all the production, operating, interest, taxes and other expenses). Using the income statement above for the year 2008, to get the net margin it would look like: $299,000 (net income) ÷ $15,500,000 (revenue or sales) = 2% net margin.

Asset Turnover = Net Sales (Revenue) ÷ Total Assets: Also known as Investment turnover. This measures a company's ability to use assets to generate sales. Although the ideal level for this ratio varies greatly, a very low figure may mean that the company maintains too many assets or has not deployed its assets well, whereas a high figure means that the assets have been used to produce good sales numbers. A ratio of 1.0 is the average, but it all really depends on the type of business. The lower the turnover usually means the higher the profit margin on the product, however the higher the turnover is to be expected on highly competitive retail stores. Using the balance sheet above for the year 2008, to get the asset turnover it would look like: $15,500,000 (revenue or sales) ÷ $685,500 (total assets) = 23 times.

Return on assets (ROA) = Net Income ÷ Total Assets: This indicates how effectively the company is deploying its assets. A very low ROA usually indicates inefficient management, whereas a high ROA means efficient management. However, depreciation or any unusual expenses can distort this ratio. It's a useful number for comparing competing companies in the same industry. Using the income sheet for net income, and the balance sheet for total assets for the year 2008, to get the ROA it would look like: $299,000 (net income) ÷ $685,500 (total assets) = 44% ROA.

Return on investment (ROI) = Net Income ÷ Owners' Equity: Also called Return on equity or ROE. This is a key measure of return for both shareholders and management. It indicates how well the company is utilizing its equity investment. Due to leverage, this measure will generally be higher than return on assets. ROI is considered to be one of the best indicators of profitability. It is also a good figure to compare against competitors or an industry average. Generally, companies usually need at least 10-14 percent ROI in order to fund future growth. If this ratio is too low, shareholders will sell their shares to invest in a company with a better return, and the Board of Directors (BOD) might have to replace management. On the other hand, a high ROI can mean that management is doing a good job, or that the firm is undercapitalized. Using the income sheet for net income, and the balance sheet for owners’ equity for the year 2008, to get the ROI it would look like: $299,000 (net income) ÷$338,500 (owners’ or shareholders equity) = 88% ROI.

By calculating ratios, you can find patterns like is the company generating cash? Is the liquidity strong? Does the company have too much debt or too many assets? Is it growing the assets faster than sales? Are the margins weak or strong? How do the ratios compare to the last couple of years, etc? You can compare ratios using industry norms published in Standard & Poor’s or Dun & Bradstreet.

It is imperative to calculate accurately on all financial statements, as these will tell you the company’s performance and creditworthiness. All red flags, such as increasing earnings and declining cash flow, should be taken seriously. Again, the goal is to be EBIT positive and you should always do your part to help get to that point and stay there.

Some other ratios that investors look at are:

- Earnings Per Share (EPS) = Net income remaining for stockholders ÷ Common shares outstanding (also considered part of the bottom line). For example, $700 (Net income) ÷ 1,000 (1,000 shares of stock) = $ 0.70

- Price Earning Ratio (PE) = Market price ÷ Earnings per share

- Dividend Payout Ratio = Dividends per share ÷ Earnings per share

- Dividend Yield Ratio = Dividends per share ÷ Current market price

The cash flow statement is a measure of a company's financial health. The cash flow statement differs from these other financial statements because it acts as a kind of corporate checkbook that reconciles the balance sheet and income statement. The cash flow statement records the company's cash transactions, both the inflows and outflows, during the given period. While an income statement can tell you whether a company made a profit, a cash flow statement can tell you whether the company generated cash. It shows whether revenues booked on the income statement have actually been collected. At the same time, however, the cash flow does not necessarily show all the company's expenses. Not all expenses the company accrues have to be paid right away. So even though the company may have incurred liabilities it must eventually pay, expenses are not recorded as a cash outflow until they are paid.

The most commonly used format for the cash flow statement is broken down into three sections:

- Cash flows from operating activities. These flows are related to your principal line of business and include the cash receipts from sales or for the performance of services, payroll and other payments to employees, payments to suppliers and contractors, rent payments, payments for utilities, and tax payments.

- Cash flows from investing activities. These are capitalized as assets on the balance sheet. Investing activities also include investments that are not part of your normal line of business. These cash flows could also include purchases of property, plant and equipment, proceeds from the sale of property, plant and equipment, purchases of stock or other securities other than cash equivalents, and proceeds from the sale or redemption of investments.

- Cash flows from financing activities. These flows relate to the businesses debt or equity financing. They include proceeds from loans, notes, and other debt instruments, installment payments on loans or other repayment of debts, cash received from the issuance of stock or equity in the business, and dividend payments, purchases of treasury stock, or returns of capital.

Cash for purposes of the cash flow statement normally includes cash and cash equivalents. Cash equivalents are short-term, temporary investments that can be readily converted into cash, such as marketable securities, short-term certificates of deposit, treasury bills, and commercial paper. The cash flow statement shows the opening balance in cash and cash equivalents for the reporting period, the net cash provided by or used in each one of the three categories just described, the net increase or decrease in cash and cash equivalents for the period, and the ending balance.

Accounting keeps track of the flow of money by keeping financial records of sales, expenses, receipts, and disbursements of cash, including calculating the taxes the company owes. An accountant’s primary function is to develop and provide data measuring the performance of the firm, assessing its financial position, and paying taxes. They are responsible for preparing financial statements such as the income statement, balance sheets, and cash flows. Some common responsibilities and controls of the accountant, also sometimes known as the controller, are:

· Accounts Receivable, which tracks the money the company is owed and paid.

· Accounts Payable, which tracks expenditures and authorizes checks to be cut to pay bills to suppliers.

· Payroll, which ensures employees get paid.

· Credit, decides just how much credit will be extended to a customer. This gives selected customers who are in good standing time to pay, whereas COD (cash on delivery) is for customers who are not in good standing due to late payments, etc.

Accountants or bookkeepers use journals or ledgers, sometimes referred to as “the books” or “the books of accounts,” to keep track of all transactions. These ledgers used to be on specially ruled ledger paper, however, accounting computer software is now more commonly used. Ledger entries can be made on a daily, weekly, monthly, or quarterly basis. It is common to have at least three ledgers: cash inflow ledger, cash outflow ledger, and the general ledger. At the end of the accounting period, the various journals and sub-ledgers are posted into the general ledger. Some common sub-ledgers are for separate kinds of transactions. For example, sales transactions in the sales ledger, payroll checks in the payroll ledger, invoice in accounts receivable ledger, and bills received in the accounts payable ledger. The financial statements we discussed earlier are drawn up from the general ledger.

These journals and ledgers will use a double-entry system. The two entries will show one debit, which would be an entry on the left hand side of an account, and one credit, which would be an entry on the right hand side of an account. These two entries offset each other and keep the books in balance:

The debit represents:

- An increase in an asset account.

- A decrease in a liability account.

- A decrease in a revenue account.

- An increase in an expense account.

The credit represents:

- A decrease in an asset account.

- An increase in a liability or owners equity account.

- An increase in a revenue account.

- A decrease in an expense account.

Once all of the transactions have been recorded and posted to the general ledger, they are then entered into the balance sheet and income statement and summed up. These are the accounts total or “Net Balances.”

The financial statements for publicly held companies require an opinion written by an independent auditor. The auditor is a CPA (certified public accountant, licensed by the state where they practice) who audited the company’s books and financial statements. If the CPA’s opinion is approved “without qualification,” then the auditor found the company is in accordance with GAAP. If the accountant’s opinion is “qualified,” then there was a practice or transaction not in accordance with GAAP, or for another reason to believe the statements do not truly reflect the company’s financial condition.

Inventory is defined as assets that are intended for sale, are in process of being produced for sale, or are to be used in producing goods. Counting inventory is done in two ways: The Periodic method, which is a physical count daily, weekly, monthly or yearly, and Perpetual inventory method, which adjusts inventory with each transaction through computerized software, such as Fishbowl inventory.

Because prices of specific items can continually change, it affects the way a manufacturer accounts for materials it buys, and how a retailer accounts for the goods it buys and then sells, which affects its cost of goods sold (COGS) and its reported income.

The following equation expresses how a company's inventory is determined:

Beginning Inventory + Net Purchases - Cost of Goods Sold (COGS) = Ending Inventory

In other words, you take what the company has in the beginning, add what they have purchased, subtract what they've sold and the result is what they have remaining.

By re-arranging the formula you can get the COGS:

Beginning Inventory + Net Purchases - Ending Inventory = Cost of Goods Sold

In other words, you take what the company has in the beginning, add what they have purchased, and subtract the inventory at the end of the period, which would then equal the amount of units sold.

FIFO, LIFO and Average Costing Method

These are three of the most common methods of accounting for inventories. Here is a brief explanation of each:

- FIFO (First in, First out. Pronounced fife-oh) - The company assumes that the first item making its way into inventory is the first sold. FIFO is used by businesses whose goods spoil quickly or frequently become obsolete. As prices go up, the FIFO method gives you the lower cost of goods sold because goods bought at the lower prices are the first to be used. This will give a better bottom line or net profit because the COGS is lower, thus gross sales is higher. With higher profits comes a higher tax bite, however, the higher income looks better to prospective investors and lenders. If prices are rising, FIFO gives a better indication of the value of ending inventory on the balance sheet. LIFO isn't a good indicator of ending inventory value, because the left over inventory might be extremely old and maybe obsolete. If prices are decreasing, which is not as common, the exact opposite of the above is true.

- LIFO (Last in, First out. Pronounced life-oh) - The company assumes that the last item making its way into inventory, or most recent, is assumed to be sold first. LIFO is used when inventory does not spoil or become obsolete. When the costs of goods rise, they first sell the more costly items. COGS will be higher, thus gross sales will be lower. Net profit will be lower, but so will the tax bite.

- Average Costing Method – This is used when COGS fluctuate frequently throughout the year. The peaks and valleys tend to even out and minimize the impact on the bottom line. It is the simplest method and doesn’t track which items are sold, but just maintains a running average of cost per unit sold.

Whichever method is used, it is important to stick to just one and not switch due to possible tax implications, unless you ask the IRS for permission to change.

Accounting for depreciation deals with adjustments that are made to company profits once a month, or once a year, to account for expenses such as depreciation and amortization. The IRS has a depreciation table that specifies the life span for various types of business equipment. See www.irs.gov for more information. The most common methods used of accounting for depreciation are:

- Straight-line depreciation = Cost of asset ÷ asset’s years of life.

- Double declining balance = Book value of the asset times twice the straight-line rate.

- Sum of the year’s digits is a method of calculating depreciation of an asset that assumes higher depreciation charges and greater tax benefits in the early years of an asset's life.